Copyright © Servias Mazhetese, 2023 All rights reserved. Written consent from the publisher is required for any reproduction, storage, or introduction into a retrieval system, or transmission of any part of this publication, whether by electronic, mechanical, photocopying, recording, or any other means. Any person who does any unauthorised act in relation to this publication may be liable for criminal prosecution and civil claims for damages.

Foreword Moore’s Law states that “Computing capability doubles every eighteen to twenty-four months while cost is halved over that timeframe.” This means that the faster computing grows, the cheaper it becomes. Since most events published in the book are up to 2021, a lot would have changed, by the time it is published.

I started drafting this book just before the onset of the Covid-19 Pandemic, took a break for about a year and then resumed thereafter. Most of the content is based on courses I undertook through the University of Nicosia, [ntroduction To Blockchain and Digital Currencies, Decentralised Finance (DeFi) and Introduction to Non-Fungible Tokens (NFTs]]. I also learnt a lot from International Telecommunications Union (ITU), 10x1000, and Dimitra Technology. Developmental events in the digital currency space are based on media reports.

Blockchain technology and digital currencies are among the most significant innovations of our time. They represent a new paradigm for how we think about trust, transparency, and security in the digital age. In just over a decade since the launch of Bitcoin, the first decentralised digital currency, blockchain and digital currencies have captured the imagination of entrepreneurs, investors, policymakers, and technologists alike.

The potential applications of blockchain technology and digital currencies are vast and varied. They offer new ways to store and transfer value, create decentralised marketplaces, enable secure and efficient payment systems, and provide new mechanisms for identity verification and data sharing. Moreover, they promise to empower individuals and communities by removing intermediaries and creating more equitable and inclusive systems.

However, with enormous potential comes great complexity and challenges. The design, implementation, and adoption of blockchain technology and digital currencies require deep technical expertise, robust governance frameworks, and careful consideration of the social, economic, and regulatory implications. As technology and its applications continue to evolve rapidly, it is crucial to have a comprehensive understanding of the underlying principles and the broader ecosystem.

In this book, I provide a clear and insightful overview of the fundamentals of blockchain technology and digital currencies, as well as the key concepts and use cases and the developments in the use of digital currency up mostly in 2021. I cover a broad range of topics, including the industrial revolution, digital adoption, blockchain technology, and digital currencies.

This book is an invaluable resource for anyone interested in learning the basics of blockchain technology and digital currencies, from beginners to seasoned professionals. It provides a solid foundation for understanding the technology and its applications, as well as the broader social, economic, and policy implications.

About the Author

Servias Mazhetese is a senior Information Communication Technology (ICT) professional with more than thirty (30) years’ experience in the industry. He has managed small to complex projects ranging from DevOps, data centre, fibre optics deployment, Contact Centre Solutions, PABX, and Mobile Network Solutions to Court Recording Technology (CRT) deployment. Servias has led projects in various sectors including ICT, finance, mining, health, and insurance.

Having been introduced to Bitcoin around 2015, and then other digital currencies, at a later stage, Servias developed a keen interest in the technology that drives these digital assets He is a DeFi, CeDeFi, TradFi, Digital Banking, AgTech, Blockchain, FinTech, IoT, ML, AI, and Robotics enthusiast.

Special Acknowledgement To my lovely wife, Brenda, for being by my side, children, Ngonidzashe “@hopetheartisgood” (for the special NFT), Mufadzi & Tinashe (for all the support).

Industrial Revolutions At the time of writing, the world had gone through four industrial revolutions, and at the initial stages of the fifth one. These are the First Industrial Revolution, (18th Century), the Second Industrial Revolution, (19th Century), the Third Industrial Revolution, (20th Century), and the Fourth Industrial Revolution, (21st Century). However, the Fifth Industrial Revolution is still at its developmental stage.

1.1. The First Industrial Revolution (IR1.0) The First Industrial Revolution started in the eighteenth century, ushering in the first steam engine. The 1st Industrial Revolution, also known as the Industrial Revolution, was a period of significant technological, economic, and social change that occurred in the late 18th and early 19th centuries in Europe and North America. It began with the invention of the spinning jenny by James Hargreaves in 1764, which led to the mechanization of textile production and the development of factory systems.

1.2. The Second Industrial Revolution (IR2.0) The Second Industrial Revolution, also known as the Technological Revolution, was a period of significant economic and technological development that occurred in the late 19th and early 20th centuries. It was characterized by a number of key inventions and innovations that transformed the way goods were produced and distributed.

One of the most important inventions of the IR2.0 was the assembly line, which was first introduced by Ransom Olds in 1901 and later perfected by Henry Ford. The assembly line made mass production more efficient and allowed for the production of standardized products at a lower cost.

Other key inventions of the 2nd Industrial Revolution included the internal combustion engine, which revolutionized transportation; the electric motor, which transformed the way factories were powered; and the telephone, which revolutionized communication.

1.3. The Third Industrial Revolution (IR3.0) The Third Industrial Revolution, also known as the Digital Revolution, refers to the period of significant technological change that began in the late 20th century and continues to the present day. It is characterized by the widespread use of digital technologies, including the internet, personal computers, and mobile devices.

A significant invention of the IR3.0 was the development of the internet, which allowed for the rapid exchange of information and the creation of new forms of communication and commerce. Other key inventions and innovations included the development of personal computers, the rise of mobile computing, and the development of social media.

The 3rd Industrial Revolution has had significant impacts on society and the economy, including the growth of e-commerce and online services, the rise of social media and digital communication, and the development of new forms of entertainment and media.

1.4. The Fourth Industrial Revolution (IR4.0) The Fourth Industrial Revolution, also known as Industry 4.0 or IR4.0, is a term used to describe the ongoing transformation of industry through the integration of digital technologies, such as artificial intelligence, the Internet of Things, robotics, and 3D printing. This revolution is considered to be a new phase in the evolution of the industrial sector, following the 3rd Industrial Revolution.

One of the key characteristics of the 4th Industrial Revolution is the use of cyber-physical systems, which combine physical systems with digital technologies. These systems are able to communicate with each other, analyse data, and make decisions in real-time.

The 4th Industrial Revolution is expected to have significant impacts on the manufacturing industry, including the development of smart factories, which are highly automated and use data and analytics to optimize production processes. It is also expected to transform other industries, such as healthcare, finance, and transportation, by creating new opportunities for innovation and growth.

The 4th Industrial Revolution is also expected to have significant social and economic impacts, including the creation of new jobs and the transformation of existing jobs, as well as changes in the way we live and work.

Overall, the IR4.0 is considered to be a major shift in the way we think about industry and technology, and it is expected to have significant impacts on society and the economy in the coming years.

1.5. The Fifth Industrial Revolution (IR5.0) The Fifth Industrial Revolution is a term that is still in its early stages of development and is not yet widely recognised or defined. Some experts predict that it will build upon the digital and technological advancements of the 4th Industrial Revolution, with a focus on new areas such as biotechnology, nanotechnology, and quantum computing. It “is going to continue to concentrate more on an innovative human-machine interface as well as not replacing human workers.”

One possible aspect of the IR5.0 is the development of bio-digital technologies, which would combine biological and digital systems to create new forms of products, services, and processes. This could include the creation of new materials and medicines, as well as new approaches to agriculture and environmental management.

Another possible area of development in the 5th Industrial Revolution is quantum computing, which would allow for the processing of vast amounts of data at incredibly high speeds. This could lead to new breakthroughs in fields such as artificial intelligence, cryptography, and materials science.

Other potential areas of development in the 5th Industrial Revolution could include the development of new energy sources and the creation of new ways of working and collaborating, such as decentralised networks and open-source platforms.

While the 5th Industrial Revolution is still largely undefined, it is clear that it will build upon the advances of the previous industrial revolutions and will continue to transform the way we live and work in the coming decades.

Digital Adoption Solutions 2.1. Digitalisation and Digitisation Digitalisation involves the utilisation of digital technologies to revolutionise a business model and generate fresh opportunities for value and revenue creation. This refers to the process of transitioning to a digital enterprise. Digitisation is changing from analogue to digital form (digital enablement). It is taking an analogue process and converting it to a digital form without actually changing the process itself. Digitalisation can also be defined as the use of digital technologies that impact many domains of economic and social life, transforming how people interact, work, and earn revenues, and digitisation as the conversion of an analogue economic sector into a digital one. According to Osman, (2018), digitalisation is restructuring many domains of social life around digital communication and media infrastructures,

Digitisation is also described as encoding analogue information into zeros and ones for computers to store, process and then turn into meaningful information. In banking, digitisation is replacing paper-based work like loan applications and converting manual controls to electronic, like in ID verification. Digitalisation is the act of making processes more automated through the use of digital. This involves credit decision engines such as for underwriting automation, identification checks with optical character recognition (authenticated IDs). While the two terms have distinct meanings, they are sometimes used interchangeably. However, Gartner’s and Planas’s definitions are more aligned with the banking environment as they relate to its business models and processes.

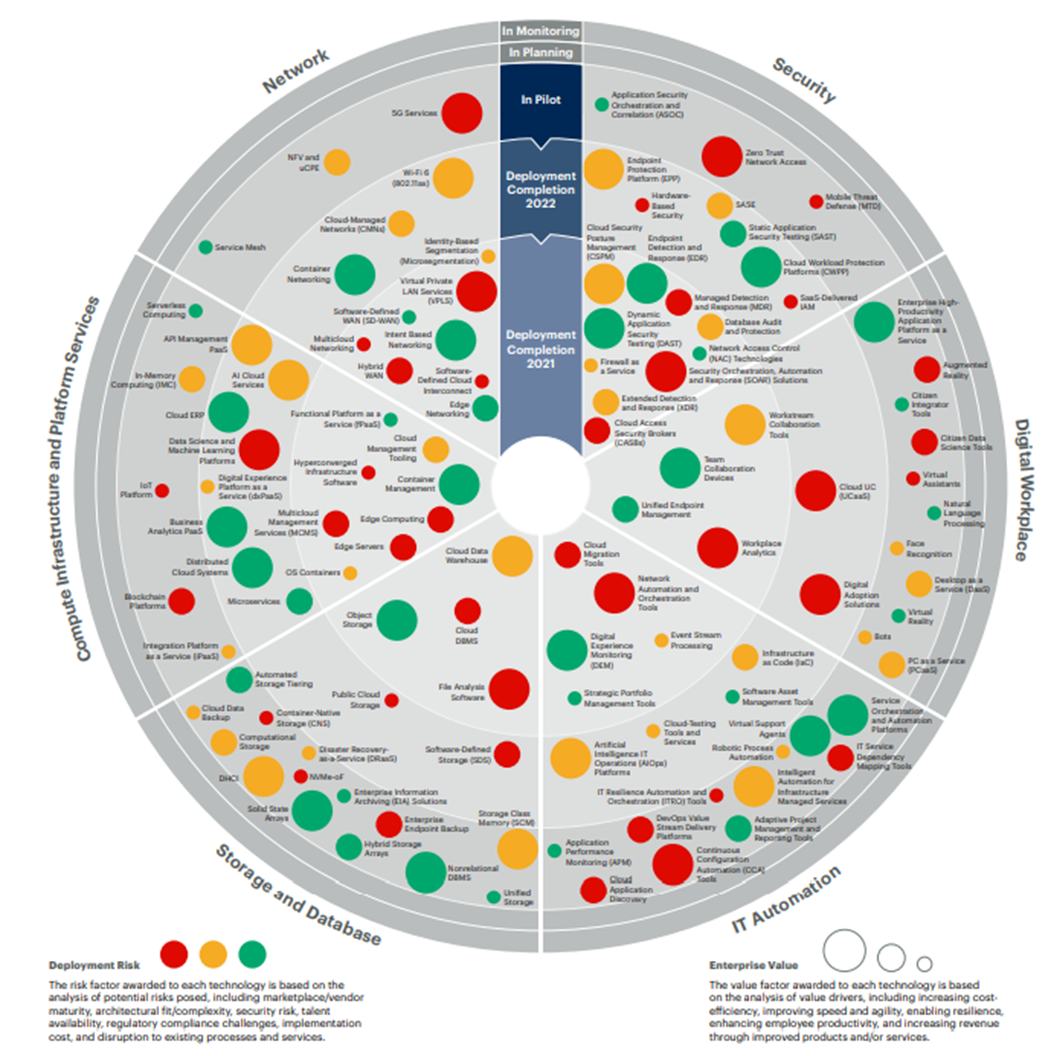

2021-2023 Gartner Emerging Technology Roadmap for Large Enterprises According to the 2021-2023 Gartner Emerging Technology Roadmap for Large Enterprises, collaborative benchmark adoption plans by IT Professionals from 437 Organisations, below are Anticipated Values and Risks for 111 Infrastructure and Operations Technologies. In the Digital Workplace, Digital Adoption Solutions remain an elevated risk.

3.1. Key Take-Aways • I&O and IT leaders have increased the adoption of emerging technologies as organizations begin to recover from the pandemic by seeking innovation opportunities. • Talent shortages are a rising and significant challenge for successful adoption of emerging technologies. • The need for resilience drives the business case for the majority of emerging technology deployments this year. • I&O leaders are placing greater significance on emerging technologies that facilitate democratized delivery. • I&O leaders are creating distributed platforms, supported by cloud technologies, which can enable an “anywhere operations’’ model for employees. • To maintain seamless access to enterprise networks and efficient delivery of network services, I&O executives are implementing highly disruptive emerging technologies. • Organizations are investing in technologies that enable intelligent data and analytics capabilities to scale enterprise-wide digital ambitions. • I&O functions are deploying enterprise technologies that can carve change in 2021, such as artificial intelligence (AI) cloud services, AI IT operations (AIOps) platforms and data science and machine learning platforms, while intelligent automation for infrastructure managed services, blockchain platforms and IoT platforms are in the pilot stage this year. • 9. Demand for new digital workplace technologies plateaued in 2021 compared to 2020 due to the maturing responses to the pandemic. • Only 12% of digital workplace technologies have moved ahead in the adoption cycle in 2021, compared with 41% in 2020.

3.2. Two Main Challenges in Financial Markets There are two main challenges in financial market. The first one is the 20-80 rule which states that only twenty percent of business in emerging markets can have access to adequate financial services. The second one is that not only a small portion has access to financial services, but financial services tend to chase money, instead of serving the real economy. Traditional financial institutions lack information about their clients and hence demand collateral to give loans. This builds trust between the lender and the borrower.

3.3. How Digital Technology Transforms Finance Digital Technology can transform finance in three ways:

It changes how financial institutions find its customers. Gone are the days when customers had to wait for the banks to be opened for them to access financial services. Now they can access these services at the palm of their hands through the mobile device connected to internet.

Due to lack of information, lending used to be collateral based. Now with abundance of information, financial institutions can make smarter lending decisions and risk management, thereby making finance easily available.

Digital technology helps to rebuild trust. With the advent of digital identity, lenders now know more of who we are thereby making it easier for them to do full KYC (Know Your Customer).

Blockchain Technology The blockchain is a type of distributed ledger that is immutable and enables the seamless recording of transactions and asset tracking across a business network. Assets that can be tracked through the blockchain include both tangible items like houses, cars, cash, and land, as well as intangible assets such as intellectual property, patents, copyrights, and branding. Anything of value can be tracked and traded on a blockchain network, reducing risk, and cutting costs for all involved.

The first blockchain simulation protocol was proposed by cryptographer David Chaum in 1982. Haber and Stornetta (2001), wrote about their work on “Consortiums,” in 1991.

Blockchain started as an idea of a support platform for Bitcoin way back in 2008. A presumed pseudonym for a person or group of people by the name “Satoshi Nakamoto” published an article called: "Bitcoin: A Peer-to-Peer Electronic Cash System" on 1 November 2008. In this article, he explained the idea of an electronic cash system based on P2P network technology, cryptography, timestamping technology and blockchain technology. Hal Finney built the first reusable proof-of-work system in 2004 after receiving ten bitcoins from Nakamoto. This marked the birth of Bitcoin. The author was introduced to bitcoin in 2016 through a community platform based on peer-to-peer (P2P) transactions.

A blockchain is a special kind of ledger that uses maths and game theory to enable: • Time stamping • Immutability • Auditability

Two fundamental properties of blockchain are immutable and distributed. The immutability aspect of blockchain means that it is always accurate and trusted, while being distributed prevents it from network attacks.

Blockchain is a peer-to-peer append-only ledger of transactions grouped into blocks, in a way that each participant can verify it on their own. Updating the ledger (usually) requires solving Byzantine Agreements with economically incentivized participation, secured by cryptography. The first Blockchain application was cryptocurrencies.

Blockchain technology is used in many industries like agriculture, healthcare, insurance, financial services, supply chain, retail, media and advertising, oil and gas, real estate, travel and transportation, and gaming.

Smart Contracts Smart contracts are self-executing contracts that are programmed to automatically execute the terms of an agreement when specific conditions are met. They are a key feature of blockchain technology, enabling the creation of decentralised applications (dApps) that run on a blockchain network.

In traditional contracts, parties rely on intermediaries such as lawyers or banks to enforce the terms of the agreement. Smart contracts eliminate the need for intermediaries by automatically executing the terms of the agreement, which are encoded in code and stored on the blockchain. This provides greater security, efficiency, and transparency in the contract execution process.

Smart contracts can be used for a variety of purposes, such as payment processing, asset transfer, supply chain management, and more. For example, a smart contract can be used to facilitate a real estate transaction. The terms of the agreement, such as the price and the conditions for transferring ownership, can be encoded in the smart contract. Once the buyer pays the agreed-upon price, the smart contract automatically transfers the ownership of the property to the buyer.

One of the key benefits of smart contracts is that they can be audited and verified by anyone on the blockchain network, providing greater transparency and reducing the potential for fraud or disputes. They can also be designed to be tamper-proof, ensuring that the terms of the agreement are executed exactly as specified.

However, there are also challenges associated with smart contracts, such as the need for robust programming skills and the potential for errors or vulnerabilities in the code. Additionally, there may be legal and regulatory challenges to the use of smart contracts, particularly in cases where there is a dispute over the interpretation or enforcement of the contract terms.

Overall, smart contracts are a powerful tool for creating more secure, efficient, and transparent business processes on a blockchain network. As technology continues to evolve and becomes more widely adopted, smart contracts are likely to play an increasingly important role in a variety of industries and applications.

Digital Currencies A digital currency is virtual money that is created in a digital format. It is not physical money. A cryptocurrency is digital money, but a digital currency is not necessarily a cryptocurrency.

6.1. Cryptocurrency 6.1.1. What is Cryptocurrency? Cryptocurrency is usually decentralised blockchain-based cryptographically created digital asset or cash that enables individuals to transact electronically. Cryptocurrencies are created autonomously without the control of a central or reserve bank. Examples of cryptocurrencies are Bitcoin (BTC), Ether (ETH), Zimbocah (ZASH), Polkadot (DOT), Binance Coin (BNB), and Litecoin (LTC).

6.1.2. Decentralised Finance (DeFi) DeFi is a term used for financial products and services that are accessible to anyone who can use Ethereum (i.e., anyone with an internet connection).

6.1.2.1. Current Challenges Addressed by DeFi • Most people are either unbanked or underbanked (or cannot use financial services). • Lack of access to financial services can prevent people from being employable. • Financial services can block one from getting paid. • A hidden charge of financial services is one’s personal data. • Governments and central banks can close down markets at will. • The trading hours are frequently restricted to the business hours of a particular time zone. • Money transfers can take days due to internal human processes. • There is a premium to financial services because intermediary institutions need their cut. 6.1.2.2. What One Can Do with DeFi • Send money around the globe. • Stream money around the globe • Access stable currencies • Borrow funds with collateral. • Borrow without collateral. • Start crypto savings. • Trade tokens • Grow one’s portfolio. • Manage one’s portfolio. • Fund one’s ideas. • Buy insurance.

6.1.3. DeFi Layers Decentralised Finance (DeFi) platforms consist of a stack of layers. These layers may include: • Settlement Layer: The blockchain – Ethereum contains the transaction history and state of accounts. • Asset Layer: ETH and the other tokens (currencies). • Protocol Layer: Smart contracts that provide the functionality, for example a service that allows for decentralised lending of assets. • Application Layer: The products we use to manage and access the protocols. • Aggregation Layer: A layer that takes input from multiple neurons or nodes in the preceding layer and combines them into a single output.

6.1.4. Bitcoin Bitcoin is a cryptographically created peer-to-peer digital currency which operates on decentralised blockchain platform, free of any control from the central banks or governments. Bitcoin transactions are recorded on a public ledger and copies are held on servers in different parts of the world. The bitcoin network came into existence on 3 January 2009, with Satoshi Nakamoto mining the genesis block of bitcoin (block number 0), which had a reward of 50 bitcoins. A few days later, on 9 January 2009, a block with the number 1 appeared and was connected to the Genesis block with the number 0 to form a chain, marking the birth of the blockchain.

6.1.5. Cryptocurrency Acceptance 6.1.5.1. El Salvador: Bitcoin as Legal Tender President Nayib Bukele passed the "Ley Bitcoin” through the Parliament of El Salvador on the 9th of June 2021. This is a law that made El Salvador, the first country in the world to officially adopt Bitcoin as its national currency (in addition to the American dollar), thereby becoming legal tender on the 7th of September 2021. On the first day of it becoming a legal tender in El Salvador, the country bought bitcoin reserves to get to 550 BTC.

At the time of writing, El Salvador had bought 150 more bitcoins and the country now holds over 700 BTC, according to its President, Nayib Bukele.

6.1.5.2. Universal Air Travel Plan (UATP) More than three hundred airline air travel members and merchants are now transacting in cryptocurrency through Universal Air Travel Plan (UATP) facilitated by Bitpay. Some of the cryptocurrencies to be accepted are bitcoin, dogecoin, ethereum, litecoin and six other popular cryptocurrencies for travel. This will enable millions of new global customers to pay regardless of which crypto wallets they use.

6.1.5.3. Zimbabwe Considering Adoption of Cryptocurrency In its weekly publication of the 7th of November 2021, The Sunday News the call by the Zimbabwean government of an adoption of cryptocurrency. It quoted the Permanent Secretary and Head of e-government Technology Unit in the Office of the President and Cabinet Retired Brigadier General Charles Wekwete speaking at a Computer Society of Zimbabwe (CSZ) Information Communication Technologies (ICT) Summit that was held in the tourist town of Victoria Falls.

6.1.5.4. Mosi Oa Tunya Gold Coin “Pursuant to the resolution of the Monetary Policy Committee of 24 July 2022 and the Bank’s Press Statement of 4 July 2022,” the Reserve Bank of Zimbabwe introduced the first 2,000 Mosi-oa-Tunya Gold Coin on 25 July 2022.

Without delving into the implementation process, the idea of introducing the gold-backed-coin, Mosi-Oa-Tunya, by the Reserve Bank of Zimbabwe, is a noble one. This clearly indicates the monetary authority’s understanding of what money is.

The gold coins were available for sale to the public from 25 July 2022 in both local currency (ZW$) and United States Dollars (US$) (and other foreign currencies) at a price based on the prevailing international price of gold plus 5% to cover the cost of production and distribution of the coin on a Payment vs Delivery basis.

Once payment has been received by the selling Agent, the buyer of the gold coin takes physical possession of the gold coin or opt to keep the gold coin through bankers of own choice (custodial services) on terms and conditions of the custodial service provider.

6.1.5.4.1. Redemption

The Bank or its Agents offer to repurchase the gold coins from the holder after a vesting period of 180 days, subject to the holder's discretion. This initiative is aimed at promoting a savings culture in the country.

For the buy-back, the Bank or its Agents shall request the bearer to surrender the original bearer certificate for the specific coin. Coins shall be purchased at the prevailing international spot price of gold.

On redemption, both residents and non-residents (international buyers), will have a choice to request payment in (US$) or (ZW$).

KYC principles will be strictly adhered to at all times.

The gold coin has the following characteristics: -

Liquid Asset Status,

Prescribed Asset Status,

Can be used as collateral,

Tradable,

Can be bought-back at the instance of the holder. The above characteristics are the real definition of money and hence I consider the Mosi-oa-Tunya to be real money. I wish the Zimbabwean government would slowly transition to the adoption of the Mosi (MoT) as its only currency.

6.1.5.5. What is Zimbocash? ZIMBOCASH is a payment wallet designed for Zimbabweans, utilizing a decentralised currency known as ZASH. ZASH is a money system that is fixed in supply. It is accessible by anyone who has a Zimbabwean ID and has access to the internet. People from other countries can buy ZASH on secondary markets on cryptocurrency exchanges. A total of 4.5 billion ZASH tokens have been issued and built on TRON decentralised platform.

While the introduction of ZASH is a noble one, the challenge with it is that it has no intrinsic value. Without intrisic vale, it remains volatile and with a speculative value.

6.1.6. Ethereum

With Ethereum technology, you can send cryptocurrency to anyone by paying a nominal fee. It is the basic settlement layer, Layer One (L1) protocols within the Decentralised Finance (DeFi) ecosystem launched in July 2015 by Vitalik Buterin and Gavin Wood. It also powers applications that everyone can use, and no one can take down. It is open-access to digital money and data-friendly services for everyone – no matter your background or location. It is the technology behind the cryptocurrency ether (ETH) built for the community.

Ethereum is the world’s programmable blockchain. It is an upgrade of Bitcoin’s innovation, though different in many ways. The major similarity is that both Ethereum and Bitcoin let one uses digital money without intermediaries like payment providers or banks. Due to its programmable nature, Ethereum can be used for other digital assets including Bitcoin itself. It allows one to move money or make agreements directly without going through intermediaries. 6.1.6.1. Characteristics of Ethereum • Open: It can be easily accessible • Borderless: It does not have boundaries • Censorship resistant: It is not prone to censorship • Immutable: Not able to be forfeited • Transparent: clear and understandable • Global: It is everywhere • Decentralised: Int is not centrally controlled

6.1.7. What is Ether (ETH)? Ether is scarce digital global money (cryptocurrency) which is the currency of Ethereum apps. 6.1.7.1. Uses of Ether • Stream ETH – receive funds in real time or pay someone. • Swap tokens – Trading with other tokens or cryptocurrency. • Earn interest – on ETH and other Ethereum-based tokens. • Get stablecoins – access the world of cryptocurrencies with a steady, less-volatile value.

6.1.8. The Scalability Trilemma The Scalability Trilemma, also known as the blockchain trilemma, is a concept that highlights the three essentials but mutually exclusive attributes of blockchain technology: security, scalability, and decentralisation.

In the context of blockchain, security refers to the ability of the system to prevent unauthorized access, tampering, or double-spending of digital assets. The concept of decentralisation entails distributing authority and decision-making among a network of nodes, as opposed to depending on a central governing body. Scalability refers to the ability of the blockchain to handle a growing number of transactions without sacrificing security or decentralisation.

The Scalability Trilemma suggests that it is impossible to achieve all three attributes at the same time. For example, increasing the number of transactions that a blockchain can handle (scalability) may require sacrificing either security or decentralisation. Likewise, enhancing the security of the blockchain may limit its ability to scale or decentralise.

Many blockchain platforms have attempted to address this trilemma by implementing various solutions, such as sharding, off-chain transactions, or consensus algorithms. However, finding the right balance between these three attributes remains a challenging problem in blockchain technology.

6.1.8.1. Stablecoins A stablecoin is a digital asset that utilises one of several technological or financial techniques, or a combination thereof, to maintain a stable price against a set target. It is a digital coin or asset backed by a stable fiat currency, asset, or commodity. A stablecoin is defined as “a fixed-price cryptocurrency whose market value is attached to another stable asset.” Unlike cryptocurrencies, a stablecoin “can be pegged to assets such as certain fiat currencies that can be traded on exchanges, including the U.S. dollar or the Euro. Some stablecoins can be pegged to other types of assets, including precious metals, such as gold, and even other cryptocurrencies.” Some examples of stablecoins are BIX Coin, backed by the United States Dollar, AFRA Coin, backed by precious minerals, African Kingdoms Lumi (AKL), underwritten completely by solar energy convertible to gold, Mosi-oa-Tunya, backed by gold, and the SAR Coin, backed by the South African Rand. A stablecoin can either be just a digital currency or a cryptocurrency.

Table 2: Top Stablecoins

6.2. Central Bank Digital Currencies (CBDC) Central bank-backed digital currencies or CBDCs and cryptocurrencies are both virtual money, though the CBDCs are legal tender regulated by central banks while cryptos are out of government control. A Central Bank Digital Currency (CBDC) is a type of digital currency supported and distributed by a central bank. With the increasing popularity of cryptocurrencies and stablecoins, central banks worldwide have recognized the need to offer an alternative or risk falling behind in the evolution of monetary systems.”

“Central Bank Digital Currency CBDC) is a digital payment instrument, denominated in the national unit of account, which is a direct liability of the central bank. A 2021 BIS survey of central banks found that 86% are actively researching the potential for CBDCs, 60% were experimenting with the technology and 14% were deploying pilot projects.”

6.2.1. What is Money? Before exploring what CBDCs are, it is imperative to define what money is first. Money is a • medium of exchange that facilitates economic transactions. • store of real value; • unit of account for the pricing of goods and services;

6.2.2. Paper Money

"Paper money eventually returns to its intrinsic value - zero." -Voltaire, 1694-1778

The history of fiat money (i.e., money issued by government decree) shows that governments consistently increase supply far beyond demand. This invariably leads to devaluation of the currency over time, something that we experience as inflation.

6.2.3. What is inflation? Inflation is a rise in prices, which can be translated as the decline of purchasing power over time. The rate at which purchasing power drops can be reflected in the average price increase of a basket of selected goods and services over some period of time. The increase in prices, usually measured as a percentage, implies that a given currency unit can purchase fewer goods and services compared to previous periods. Inflation can be contrasted with deflation, which occurs when prices decline and purchasing power increases.

Certain assets, such as GOLD are more or less affected by inflation. Cryptocurrencies and digital assets like Bitcoin are peddled as hedges against inflation too.

The U.S. dollar has lost 96% of its value since 1913.

The euro has lost 40% of its value since 1997.

The British Pound has lost 99.602% of its value since 1751.

Unlike dollars, there will only ever be 21 million Bitcoin. “While fiat currencies have no upper limit to their supply, Bitcoin’s supply limit is set in stone at 21 million coins, over 90% of which are already in circulation.” (Bitcoin, 2023)

Many countries and central banks have taken the initiative to research, pilot or introduce CBDC, with ECO-6 taking the lead with by distributing its currency, African Kingdoms Lumi (aka, LUMI, or AKL) to over one million users at the time of writing this book. China and Nigeria introduced their CBDCs, e-Yuan and eNaira, respectively. In Africa, Nigeria has taken the lead with the deployment of its CBDC on the 1st of October 2021 and Ghana following suit very soon.

Ghana is muting piloting its digital eCedi while South Africa is involvement with the BIS (Bank of International Settlements)’s pilot project. As per the September 2, 2021, press release by a group of global regulators including the BIS Innovation Hub, Reserve Bank of Australia, Monetary Authority of Singapore, Bank Negara Malaysia, and South African Reserve Bank, the objective is to create experimental collaborative systems for cross-border transactions utilizing various central bank digital currencies (CBDCs). According to another press release, the Reserve Bank of South Africa is also conducting a feasibility study into CBDCs.

6.2.3.1. Some Common Motivations for CBDC There are several potential advantages of Central Bank Digital Currency (CBDC), which include:

Financial inclusion: CBDC has the potential to improve financial inclusion by providing access to banking services to those who are currently excluded from the traditional banking system.

Reduced transaction costs: Digital currency transactions are cheaper than traditional payment methods, such as credit cards or wire transfers. This could result in lower transaction costs for consumers and businesses.

Increased efficiency: CBDC could improve the efficiency of the payment system by reducing settlement times and increasing the speed of transactions.

Greater transparency: CBDC could enhance the transparency of the payment system by providing real-time transaction data that can be used to track and monitor financial activity.

Reduced counterfeiting: Digital currency transactions are more difficult to counterfeit than traditional currency, which could help to reduce fraud and counterfeiting.

Monetary policy effectiveness: CBDC could provide central banks with greater control over monetary policy by enabling them to monitor transactions in real-time and respond more quickly to changes in the economy.

Reduced reliance on cash: CBDC could reduce the use of physical cash, which could lead to a reduction in the underground economy and help to combat money laundering and tax evasion.

6.2.3.2. Disadvantages of CBDC There are several potential disadvantages of Central Bank Digital Currency (CBDC), which include:

Cybersecurity risks: Digital currencies are vulnerable to cyber-attacks, and a CBDC is no exception. If hackers were to gain unauthorized access to the system, it could result in a significant loss of funds.

Financial disintermediation: A CBDC could lead to disintermediation, meaning that it may reduce the role of banks as intermediaries between savers and borrowers. This could have negative implications for financial stability and the credit system.

Negative impact on bank deposits: If a CBDC becomes more popular than traditional bank deposits, it could result in a reduction in bank deposits. This could have a negative impact on banks' ability to provide loans and finance economic growth.

Privacy concerns: The use of a CBDC could pose a threat to individual privacy. The central bank would be able to track every transaction, which could lead to concerns about government surveillance and the misuse of personal data.

Implementation costs: The implementation of a CBDC could be expensive, as it would require significant investment in infrastructure and technology.

Technical challenges: The development and implementation of a CBDC would require significant technical expertise and resources. It may also face technical challenges such as scalability, interoperability, and cybersecurity.

6.2.4. AKL: African Kingdoms Lumi (Lumi) 6.2.4.1. LUMI Currency The two major challenges of finance are that it is not inclusive and does not serve the real economy very well. The Lumi seeks to address these challenges.

The Africa Diaspora Central Bank (ADCB) is responsible for issuing the LUMI, which is the official currency of the Sixth (6th) Region of the Economic Community of the African Diaspora. The member state financial institutions of the ADCB also issue this currency. In January 2021, the African Finance Regulatory Authority (AFRA) Commission recognized the LUMI as legal tender for continental Africa. The LUMI was created by a Canadian-born Jamaican H.M. Rex Semako I & VI Chief Timothy Elisha McPherson. He is also The Chairman of the Economic Community of States, Territories & Realms of the African Diaspora Sixth Region (ECO-6) and President and Governor of ADCB. The author of this book is the introducer of ECO-6 to Swifin, the digital platform distributing the LUMI.

The LUMI derives its name from the word “LUMINOUS” symbolising the Sun (Ra). The currency is backed by solar energy and gold. Solar energy is the best source of energy for Africa’s economic development and environmental protection mandate. The LUMI is both a physical currency as well as a central bank digital currency (CBDC).

6.2.4.2. LUMI Stimulus ECO-6 is issuing a LUMI economic stimulus valued at US$100 (the equivalent of 6.26 LUMI) per person per month paid direct to their wallet for a period of 3 years (US$1200 per year). The first stimulus was issued on the 28th of October 2020. The objective of this stimulus is to promote socio-economic growth by fostering economic development across all African kingdoms, nations, territories, and the Diaspora. It is a Pan-African initiative aimed at encouraging progress in the region. (Eco-6, 2021). All Africans in the Diaspora and all Africans on the Continent over the age of eighteen (18) years, (13 years in Eswatini and some other selected countries), started receiving the stimulus once registered on the Swifin Platform. At the time of writing, there were over one million recipients.

The LUMI not a cryptocurrency but a classic digital currency. It is underwritten by 100KWh of solar energy and convertible to four (4) grains of gold which is equals to 0.2592 grams. The current value for 1 LUMI is US$15.96.

6.2.5. eNaira

6.3. Digital Currencies Platforms

6.3.1. Pan-African Payment and Settlement System (PAPSS) The Pan-African Payment and Settlement System (PAPSS) was launched for operational use by Afreximbank and AfCFTA.

6.3.2. Swifin Banking Platform Swifin is an open distributed Banking Service Exchange which powers the delivery of direct and agency Digital Financial Services to both the banked and unbanked around the world via regulated strategic service Partners in different jurisdictions. It is a multi-tenant core banking and web shop platform with real time payment collection service.

6.3.2.1. Swifin Partners and Service Providers The Swifin Platform is a Financial Inclusion Ecosystem of Internet of Things (IoT) for the Unbanked, Underbanked and the Underserved (3Us) members of the community. Regulated member institutions and Digital Financial Services Providers such as Banks, Microfinance Institutions, Credit Unions and Community Savings and Loans Organisations leverage the Swifin Platform to deliver real time payments and related merchant services for platform members in real time to drive financial inclusion and active participation in the modern global digital economy. Companies and entrepreneurs around the globe are working to participate in the economic opportunity that IoT products and services can represent.

Swifin is one of the few digital banking platforms that provides inclusive financial services. This means that the services are easily accessible, affordable, sustainable and many.

*

7.1. What is a Non-Fungible Token (NFT)? A non-fungible token (NFT) also known as crypto collectible is a type of cryptographic token which is either entirely a digital asset or tokenized version of real-world distinctive asset on a blockchain. An NFT is not interchangeable with another and can be used as proof of authenticity and ownership within the digital sphere. NFTs are unique and limited in quantity, unlike cryptocurrencies.

NFTs are used in gaming, digital identity, licensing, certificates, and fine art. They allow sectional title to high-value items.

Fungible items are objects that can be interchanged and have the same value. For example, a $5 bill has the same value as other $5 bills. However, if you have a $5 bill with Elon Musk’s autograph, it is no longer fungible because it is unique and has a different value than other $5 bills. (Amaral & Rodrigues, 2023). My daughter’s art (Figure 46) in this book may not be worth anything to the reader, but it is worth a lot to me.

7.2. NFTs in Art Some of the Zimbabwean artists who have embraced NFTs are Greatjoy Ndlovu, Nyasha Warambwa and Indigo Saint, by selling their artefacts digitally on Blockchain.

7.3. Characteristics of NFTs • They are unique. • They all look the same but with unique features. • Ideal for making digital forms of collectables like art or trading cards. • Other use-cases are digital identities and real estate ownership. • They are often based on ERC721 Ethereum Blockchain tokens. • These tokens can be bought and sold on second-hand marketplaces.

Gossary

Bitpay: Bitpay is a global payment service provider that enables businesses to accept Bitcoin and other cryptocurrencies as payment for goods and services. Founded in 2011, Bitpay provides a variety of services including payment processing, cross-border payments, and cryptocurrency wallet integration.

BTC: In 2009, an individual or group of people operating under the pseudonym Satoshi Nakamoto developed Bitcoin, a digital currency that operates in a decentralised manner. BTC is the abbreviation for Bitcoin. Bitcoin operates on a peer-to-peer network, meaning that transactions are processed and verified by a decentralised network of computers, rather than a central authority such as a government or financial institution

Byzantine Agreement: Requirement for a set of parties in a distributed environment to agree on a value even if some of the parties are corrupted. It refers to a problem in distributed computing where a group of participants must come to a consensus or agreement on a value, despite the possibility of some participants behaving in a faulty or malicious manner. The problem is named after the Byzantine general’s problem, a thought experiment where a group of Byzantine generals must coordinate their actions during a military campaign despite the possibility of traitors among their ranks.

Fungible Token: A type of digital asset that is interchangeable with other units of the same type and is therefore considered to be uniform and identical in value. Fungible tokens are typically used in blockchain-based systems to represent digital assets such as currency, commodities, or other types of financial instruments. The term "fungible" means that each unit of the token is identical and can be exchanged for any other unit of the same type. This means that one unit of a fungible token has the same value as any other unit of the same token, and there is no distinction between individual units of the token.

IoT: Internet of Things: (IoT]. This sentence describes a worldwide framework that facilitates the use of cutting-edge services by linking physical and virtual objects through interoperable information and communication technologies, both current and emerging.

KYC: KYC stands for "Know Your Customer" and refers to the process of verifying the identity of customers before providing them with products or services. The KYC process is used by businesses and financial institutions to prevent money laundering, terrorist financing, and other financial crimes. KYC involves collecting and verifying a customer's personal and financial information, such as their name, address, date of birth, and government-issued identification documents. This information is used to assess the customer's risk profile and to comply with regulatory requirements. The KYC process may vary depending on the type of business and jurisdiction, but it typically involves gathering information through identification documents, verifying the information, and monitoring the customer's transactions over time.

Ley Bitcoin: A law that made El Salvador, the first country in the world to officially adopt Bitcoin as its national currency (in addition to the American dollar), thereby becoming legal tender on the 7th of September 2021.

NFT: Non-Fungible Token also known as crypto collectible is a type of cryptographic token which is either entirely a digital asset or tokenized version of real-world distinctive asset on a blockchain.

Sharding: Sharding is a database partitioning technique in which data is horizontally divided into multiple smaller parts or shards, each containing a subset of the data. This allows for parallel processing of queries and improved performance for large-scale databases.

In a sharded database, each shard can be stored on a separate server or node, enabling the database to handle more data and queries. Sharding is often used in distributed systems to improve scalability, availability, and performance.

However, sharding also introduces some complexities, such as ensuring data consistency across shards, managing shard distribution, and handling failures or node crashes. As a result, careful planning and design are required to implement sharding effectively.

UATP: Universal Air Travel Plan. Airlines in the UATP network Currently, UATP’s members include Aeromexico, Airplus International (British Airways and Lufthansa), APG Airlines, Air Canada, Air China, Air New Zealand, Air Niugini, American Airlines, APG Airlines, Austrian Airlines, BCD Travel, China Eastern Airlines, Delta Air Lines, EL AL Israel Airlines, Etihad Airways, Fareportal, Frontier Airlines, GOL Linhas aereas inteligentes S.A., Hahn Air, High Point, Japan Airlines, Jetblue, Malaysia Airlines, Qantas Airways, Shandong Airlines, Sichuan Airlines, Southwest, Sun Country Airlines, Transavia Airlines, Tuifly GmbH, Turkish Airlines, United Airlines, and Westjet.

Bibliography 10x1000. (2021, December 29). my/vod?programId=6962b19662ab47615e84e37f41105eca&programSectionId=a9b7dcaf87183d0ed6464db73bf3897d. Retrieved from https://www.10x1000.org: https://www.10x1000.org/my/vod?programId=6962b19662ab47615e84e37f41105eca&programSectionId=a9b7dcaf87183d0ed6464db73bf3897d Afreximbank. (2021, September 28). afreximbank-and-afcfta-announce-the-operational-roll-out-of-the-pan-african-payment-and-settlement-system-papss/. (Afreximbank) Retrieved March 14, 2022, from https://www.afreximbank.com: https://www.afreximbank.com/afreximbank-and-afcfta-announce-the-operational-roll-out-of-the-pan-african-payment-and-settlement-system-papss/ Amaral, T., & Rodrigues, K. (2023, March 03). tiagoamaral.eth/Qce_7MVDZBXW4wdMgFGqq1MTmT5dS50LIBUubFpSaFU. Retrieved March 23, 2023, from https://mirror.xyz: https://mirror.xyz/tiagoamaral.eth/Qce_7MVDZBXW4wdMgFGqq1MTmT5dS50LIBUubFpSaFU Atlantic Council. (2023, March 22). cbdctracker/. Retrieved from https://www.atlanticcouncil.org: https://www.atlanticcouncil.org/cbdctracker/ Bank of International Settlements (BIS). (2023, March 22). about/bisih/topics/cbdc.htm. Retrieved from https://www.bis.org: https://www.bis.org/about/bisih/topics/cbdc.htm Binance Academy. (2018, 12 05). en/articles/what-is-cryptocurrency. Retrieved 09 11, 2021, from academy.binance.com: https://academy.binance.com/en/articles/what-is-cryptocurrency Binance Academy. (2020, 02 26). en/articles/a-guide-to-crypto-collectibles-and-non-fungible-tokens-nfts. Retrieved 09 10, 2021, from academy.binance.com/: https://academy.binance.com/en/articles/a-guide-to-crypto-collectibles-and-non-fungible-tokens-nfts Bing. (2022, December 22). images/search?view=detailV2&ccid=%2b90vH6OX&id=BD2288DCDE48E13086D33B9430E3B685B6E66C99&thid=OIP.-90vH6OX2GqNvC4QtXHoXQHaEK&mediaurl=https%3a%2f%2fafropulp.com%2fwp-content%2fuploads%2f2021%2f11%2fe-naira-1.jpeg&cdnurl=https%3a%2f%2ft. Retrieved from https://www.bing.com: https://www.bing.com/images/search?view=detailV2&ccid=%2B90vH6OX&id=BD2288DCDE48E13086D33B9430E3B685B6E66C99&thid=OIP.-90vH6OX2GqNvC4QtXHoXQHaEK&mediaurl=https%3A%2F%2Fafropulp.com%2Fwp-content%2Fuploads%2F2021%2F11%2Fe-naira-1.jpeg&cdnurl=https%3A%2F%2Ft Bitcoin. (2023, March 22). get-started/what-is-inflation. Retrieved from https://www.bitcoin.com: https://www.bitcoin.com/get-started/what-is-inflation/ Chen, D. L. (2021, December 06). my/vod?programId=6962b19662ab47615e84e37f41105eca&programSectionId=a9b7dcaf87183d0ed6464db73bf3897d. Retrieved 12 08, 2021, from https://www.10x1000.org: https://www.10x1000.org/my/vod?programId=6962b19662ab47615e84e37f41105eca&programSectionId=a9b7dcaf87183d0ed6464db73bf3897d Chima, O. (2021, September 27). index.php/2021/09/27/ahead-of-october-launch-enaira-platform-goes-live/. Retrieved September 27, 2021, from https://www.thisdaylive.com: https://www.thisdaylive.com/index.php/2021/09/27/ahead-of-october-launch-enaira-platform-goes-live/ Conron, C. (2021, 11 18). blog/post/inflations-impact-on-life-insurance. Retrieved March 23, 2023, from https://app.lifedesignanalysis.com: https://app.lifedesignanalysis.com/blog/post/inflations-impact-on-life-insurance Darlington, N. (2021, November 25). guides/what-is-blockchain-technology/. Retrieved December 08, 2021, from https://blockgeeks.com: https://blockgeeks.com/guides/what-is-blockchain-technology/ Digital Money. (2023, March 23). topic/76504-what-companies-like-bitcoin-should-i-invest-in/. Retrieved from https://www.digitalmoneytalk.com: https://www.digitalmoneytalk.com/topic/76504-what-companies-like-bitcoin-should-i-invest-in/ Eco-6. (2021, December 12). lumi-currency. Retrieved from https://www.eco-6.com: https://www.eco-6.com/lumi-currency Ekekwe, N. (2021, September 27). nigeria-unveils-e-naira-website-expect-cash-to-fade-over-time/. (Tekedia) Retrieved January 15, 2022, from https://www.tekedia.com: https://www.tekedia.com/nigeria-unveils-e-naira-website-expect-cash-to-fade-over-time/ Ethereum. (2021, October 25). en/defi/. Retrieved October 25, 2021, from https://ethereum.org: https://ethereum.org/en/defi/ Ethereum. (2021, October 25). en/defi/#what-is-defi. Retrieved October 25, 2021, from https://ethereum.org: https://ethereum.org/en/defi/#what-is-defi Ethereum. (2021, October 25). en/stablecoins/#explore. Retrieved October 26, 2021, from https://ethereum.org: https://ethereum.org/en/stablecoins/#explore Ethereum. (2021, October 25). en/what-is-ethereum/. Retrieved October 25, 2021, from https://ethereum.org: https://ethereum.org/en/what-is-ethereum/ Etherium. (2023, March 23). en/defi/. Retrieved from https://ethereum.org: https://ethereum.org/en/defi/ European Migration Network. (2022, February 01). migration/mig/EMN-OECD-INFORM-FEB-2022-The-use-of-Digitalisation-and-AI-in-Migration-Management.pdf. Retrieved March 23, 2023, from https://www.oecd.org: https://www.oecd.org/migration/mig/EMN-OECD-INFORM-FEB-2022-The-use-of-Digitalisation-and-AI-in-Migration-Management.pdf Fernando, J. (2023, 03 14). terms/i/inflation.asp. (Investopedia) Retrieved March 22, 2023, from https://www.investopedia.com: https://www.investopedia.com/terms/i/inflation.asp George, A. S., & George, A. H. (2020, September 01). INDUSTRIAL REVOLUTION 5.0: THE TRANSFORMATION OF THE MODERN MANUFACTURING PROCESS TO ENABLE MAN AND MACHINE TO WORK HAND IN HAND. Journal of Seybold Report, 15(9), 215. doi:10.5281/zenodo.6548092 Getty Images. (2023, March 22). ?q=Paper+money+image&atb=v360-1&ia=web. Retrieved from https://duckduckgo.com: https://duckduckgo.com/?q=Paper+money+image&atb=v360-1&ia=web Haber, S., & Stornetta, W. S. (2001, May 18). How to Time-Stamp a Digital Document. Retrieved December 08, 2021, from https://www.anf.es: https://www.anf.es/pdf/Haber_Stornetta.pdf Helms, K. (2021, 09 20). el-salvador-buys-more-bitcoin-country-now-holds-700-btc/. Retrieved 09 20, 2021, from https://news.bitcoin.com: https://news.bitcoin.com/el-salvador-buys-more-bitcoin-country-now-holds-700-btc/ Helms, K. (2021, 09 07). first-day-bitcoin-legal-tender-el-salvador-buys-the-dip-countrys-btc-stash-grows/. Retrieved 09 20, 2021, from https://news.bitcoin.com: https://news.bitcoin.com/first-day-bitcoin-legal-tender-el-salvador-buys-the-dip-countrys-btc-stash-grows/ Helms, K. (2021, 09 10). many-major-airlines-can-now-accept-cryptocurrencies-via-uatp-global-payment-network/. (Bitcoin.com) Retrieved 09 10, 2021, from news.bitcoin.com: https://news.bitcoin.com/many-major-airlines-can-now-accept-cryptocurrencies-via-uatp-global-payment-network/ Hofacker, R. (2021, 09 20). pulse/bitcoin-legal-tender-el-salvador-wind-change-ralph-hofacker/. Retrieved 09 20, 2021, from https://www.linkedin.com: https://www.linkedin.com/pulse/bitcoin-legal-tender-el-salvador-wind-change-ralph-hofacker/ IBM. (2023, March 23). topics/blockchain. Retrieved from https://www.ibm.com: https://www.ibm.com/topics/blockchain International Telecommunication Union. (2021, August 16). mod/folder/view.php?id=22833. Retrieved September 14, 2022, from https://academycourses.itu.int: https://academycourses.itu.int/mod/folder/view.php?id=22833 Lumi Currency. (2023, March 23). https://lumicurrency.org/. Retrieved from https://lumicurrency.org/: https://lumicurrency.org/ lumi-currency. (2021, October 28). Retrieved October 28, 2021, from https://www.eco-6.com: https://www.eco-6.com/lumi-currency Mazhetese, H. N. (2023, March 23). hopetheartisgood/. Retrieved from https://www.instagram.com: https://www.instagram.com/hopetheartisgood/ Modex. (2019, October 10). a-brief-overview-of-the-scalability-trilemma/. Retrieved October 29, 2021, from https://modex.tech: https://modex.tech/a-brief-overview-of-the-scalability-trilemma/ Ncube, L. (2021, November 7). govt-considers-another-currency/. (The Sunday News) Retrieved November 7, 2021, from https://www.sundaynews.co.zw: https://www.sundaynews.co.zw/govt-considers-another-currency/ Osman, T. (2018, October 5). article/0012227-digitisation-vs-digitalisation-what-it-means-your-business. (IDM) Retrieved September 14, 2022, from https://idm.net.au: https://idm.net.au/article/0012227-digitisation-vs-digitalisation-what-it-means-your-business Planas, R. (2022, August 13). assets/61afb14666c2c0ed4d81460bc3d2cb64.pdf. Retrieved September 14, 2022, from https://edximg.oss-ap-southeast-1.aliyuncs.com: https://edximg.oss-ap-southeast-1.aliyuncs.com/assets/61afb14666c2c0ed4d81460bc3d2cb64.pdf Reserve Bank of Zimbabwe (RBZ). (2022, July 25). documents/press/2022/July/Press-Satement-on-Gold-Coins---25-July-2022-1-1.pdf. Retrieved March 22, 2023, from https://www.rbz.co.zw: https://www.rbz.co.zw/documents/press/2022/July/Press-Satement-on-Gold-Coins---25-July-2022-1-1.pdf Reserve Bank of Zimbabwe. (2022, August 23). documents/Mosi-Rates/2022/August/MOSI-OA-TUNYA-PRICES-23-AUGUST-2022.pdf. Retrieved March 22, 2023, from https://www.rbz.co.zw: https://www.rbz.co.zw/documents/Mosi-Rates/2022/August/MOSI-OA-TUNYA-PRICES-23-AUGUST-2022.pdf Reuters. (2021, August 11). https://www.reuters.com/article/ghana-cenbank-currency-idUKL1N2PI0M1. (Reuters) Retrieved December 19, 2021, from https://www.reuters.com/article/ghana-cenbank-currency-idUKL1N2PI0M1: https://www.reuters.com/article/ghana-cenbank-currency-idUKL1N2PI0M1 Rosencrance, L. (2022, September 23). whatis/definition/stablecoin. Retrieved September 23, 2022, from https://www.techtarget.com: https://www.techtarget.com/whatis/definition/stablecoin Satoshi. (2023, March 23). satoshi. Retrieved from https://www.satoshihouse.com: https://www.satoshihouse.com/satoshi Schmolze, R. (2021). 2021-2023 Emerging Technology Roadmap for Large Enterprises. Gartner. Sephton, C. (2021, 03 12). what-are-nft-tokens?utm_medium=cpc&utm_source=googledisplay_desktop&utm_campaign=Africa_MEME_PFM_EN&utm_term=&gclid=CjwKCAjwhOyJBhA4EiwAEcJdcVmmvozuwsdUZEpIhSp3opAlJqI24VhMYY2Uap2um1GxM4KrsqRpyBoC9vIQAvD_BwE. Retrieved 09 10, 2021, from currency.com: https://currency.com/what-are-nft-tokens?utm_medium=cpc&utm_source=googledisplay_desktop&utm_campaign=Africa_MEME_PFM_EN&utm_term=&gclid=CjwKCAjwhOyJBhA4EiwAEcJdcVmmvozuwsdUZEpIhSp3opAlJqI24VhMYY2Uap2um1GxM4KrsqRpyBoC9vIQAvD_BwE South African Reserve Bank. (2021, May 25). https://www.resbank.co.za/content/dam/sarb/publications/media-releases/2021/cbdc-/Feasibility study for a general-purpose retail central bank digital currency.pdf. Retrieved January 20, 2022, from https://www.resbank.co.za/content/dam/sarb/publications/media-releases/2021/cbdc-/Feasibility study for a general-purpose retail central bank digital currency.pdf: https://www.resbank.co.za/content/dam/sarb/publications/media-releases/2021/cbdc-/Feasibility study for a general-purpose retail central bank digital currency.pdf Tardi, C. (2022, July 17). https://www.investopedia.com/terms/m/mooreslaw.asp. (M. Cheng, Editor, A. Jackson, Producer, & Investopedia) Retrieved March 16, 2023, from https://www.investopedia.com/terms/m/mooreslaw.asp: https://www.investopedia.com/terms/m/mooreslaw.aspv Token Pocket. (2021, July 29). en/blockchain-basics/blockchain-definition. Retrieved October 29, 2021, from https://help.tokenpocket.pro/: https://help.tokenpocket.pro/en/blockchain-basics/blockchain-definition University of Nicosia. (2021, October 25). DeFi Infrastructure - Ethereum. BLOC 611: Introduction to Decentralised Finance- Week 1 Session 2, p. 6. University of Nicosia. (2021, October 29). Stablecoins. BLOC 611: Introduction to Decentralised Finance (DeFi). Nicosia, Nicosia, Cyprus: University of Nicosia. Walkme Digital Adoption Institute. (2022, December 19). https://institute.walkme.com/. Retrieved Decemebr 19, 2022, from https://institute.walkme.com/: https://institute.walkme.com/ Zimbo Cash. (2022, October 24). wp-content/uploads/ZIMBOCASH-Whitepaper-24-October-2022.pdf. Retrieved March 23, 2023, from https://www.zimbo.cash: https://www.zimbo.cash/wp-content/uploads/ZIMBOCASH-Whitepaper-24-October-2022.pdf Zimbocash. (2021, December 08). wp-content/uploads/ZIMBOCASH-Whitepaper-1.8.2021.pdf. Retrieved from https://www.zimbo.cash: https://www.zimbo.cash/wp-content/uploads/ZIMBOCASH-Whitepaper-1.8.2021.pdf Zimwara, T. (2021, 09 10). more-zimbabwean-artists-pivot-to-nfts-as-bubble-concerns-grow/. Retrieved 09 10, 2021, from news.bitcoin.com: https://news.bitcoin.com/more-zimbabwean-artists-pivot-to-nfts-as-bubble-concerns-grow/