Subscribe to Curve Finance Unofficial

<100 subscribers

Support Curve Finance Unofficial

CURVE FINANCE: 2025 YEAR IN REVIEW

Share Dialog

Share Dialog

Happy New Year 2026! Thank you to the community for your support — together we are building the future of DeFi.

As we reflect on 2025, let's highlight the key milestones and inspiring achievements.

A year ago, Curve generated 1.6% of DEX fees on Ethereum. Today it's 44%. A 27x increase in 12 months.

In 2024, we launched LlamaLend and scrvUSD. In 2025, these products transformed the market and became the foundation for new breakthroughs. The launch of Yield Basis turned Curve into the largest Bitcoin liquidity hub. crvUSD supply tripled to $331M. FXSwap opened the door to on-chain forex.

While dominating Ethereum, the protocol continued its multi-chain expansion — nine new networks in one year, thanks to the simplicity and convenience of Curve-Lite.

These and many other important events are covered in this report — quarter by quarter.

Q1

Q2

Q3

Q4

Q1 set the pace for the entire year. $35 billion in trading volume — the best quarter in protocol history at that time. Transactions tripled: from 1.8M to 5.5M. A record achieved against a 20% market downturn. LlamaLend doubled its TVL to $84M thanks to the Resupply launch. crvUSD gained $80M in new capacity through Bitcoin collaterals. JPMorgan forecasted yield-bearing stablecoins to grow from 6% to 50% of the market — with scrvUSD in focus. Aragon integrated the ve-model into their toolkit. The industry acknowledged: Curve technology is the standard.

January 7 — Curve deployed on Sonic — a high-performance L1 with 10,000+ TPS. Curve provided critical DEX infrastructure from day one of the network's operation.

February 17 — LlamaRisk launched Market Health Scores — seven market health metrics for crvUSD. Clear risks for LPs, predictability for borrowers, objective foundation for the DAO.

March 12 — crvUSD received three new collaterals and $80M in capacity: cbBTC (50M), weETH (20M), LBTC (10M). Two Bitcoin collaterals strengthened crvUSD's position as the stablecoin for BTC holders.

March 20 — Resupply Protocol launched — a subDAO from Convex and Yearn. The mechanics are elegant: crvUSD deposits in LlamaLend continue to earn yield and CRV incentives (with boost via Convex), while simultaneously serving as collateral for minting reUSD.

First week: $44.7K in fees, $35M reUSD minted against $42M collateral. By April, total fees reached $345K. The flywheel spun up — demand for scrvUSD pushed LlamaLend TVL from $38M to $84M in a matter of days.

March 27 — JPMorgan analysts forecasted yield-bearing stablecoins to grow from 6% to 50% of the market. The driver — the ability to earn yield without trading or lending risks. scrvUSD — the yield-bearing wrapper of crvUSD — is positioned at the center of this trend.

March 27 — Aragon integrated Curve's ve-model into their Value Accrual Toolkit. Vote Escrow (locking tokens for votes) and Gauges (distributing incentives through voting) — key components borrowed from Curve. The toolkit is already used by Mode, Puffer, Bedrock. Curve technologies have become the industry standard.

Q2 put Curve to the test. Two security incidents — an X account hack and a DNS attack — didn't stop the protocol: $400M in volume was processed while the frontend was unavailable. Meanwhile, LlamaLend showed explosive growth: TVL +228%, borrowed volume +104.5%. Three new networks, veCRV whitelist removal, record crvUSD supply. A quarter that hardened the ecosystem.

Strategic USD Reserves: New Foundation

In April, the DAO voted to adopt the USDC/USDT pool as the official Basepool — the foundation for creating new stablecoin pools called Strategic Reserves.

This was a strategic move. The old 3pool (DAI/USDC/USDT) served as the ecosystem's foundation for years, but MakerDAO migrated from DAI to USDS. Time for an upgrade.

The new Basepool uses StableSwap-NG with an amplification coefficient of 20,000 (versus ~2,000 for 3pool) — an order of magnitude more concentrated liquidity. Fees reduced to 0.003%.

Result: the pool processes ~$27M in daily volume with only $6.3M TVL — capital efficiency of 4-5x.

crvUSD: Record Supply

May 8 — crvUSD reached $179.8M in circulation — a record at the time (soon to double again). A week later, the stablecoin celebrated its 2nd anniversary.

For Curve, this isn't just a number: every minted crvUSD generates borrowing fees that go to veCRV holders. More supply — more revenue for the ecosystem.

May 26 — The DAO voted to remove the veCRV whitelist — now any smart contract can lock CRV. Previously, only Convex, Yearn, and StakeDAO participated in the ve-mechanism.

Democratization strengthens the flywheel: more protocols locking CRV → stronger demand → higher value for all holders.

Q2 brought new launches on three networks: May 27 — Plume Network (RWAfi L1), June 6 — Hyperliquid (perpetual trading L1), June 12 — XDC Network (enterprise trade finance).

Q2 was a turning point for Curve lending. According to the LlamaRisk report, borrowed crvUSD volume grew by 104.5% (from $33.5M to $68.7M). Average LlamaLend TVL increased by 228% — from $46M in Q1 to $151M in Q2.

By the end of June, borrowed volume reached $126M with 766 active positions. LlamaLend became one of the most efficient and affordable lending platforms in DeFi — large borrowers migrated for competitive rates, liquidation protection, and high capital efficiency.

Technical improvements: EMAMonetaryPolicy for markets with yield-bearing assets, ProxyOracle for flexible deployment of new markets. crvUSD peg stability improved by 66% — daily deviation reduced to 3.9 BPS. By year-end, active loans exceeded $300M.

Q2 will be remembered not only for innovations. Two security incidents — and neither stopped the protocol.

X Account Hack

May 5 — Attackers gained access to the official @CurveFinance account on X and posted a phishing link to the "first CRV airdrop." Founder Michael Egorov responded immediately: "Confirmed: Curve X account hacked." Control was restored the same day.

DNS Attack: A Turning Point

May 12 — Attackers gained access to the DNS registrar and redirected curve.fi traffic to a phishing site.

But here's the remarkable part: while the frontend was unavailable, the protocol processed over $400M in volume. Contracts continued working. The team migrated to a new domain curve.finance. The incident became an impetus for infrastructure strengthening.

March 11 — Roman Agureev, a Curve researcher, discovered a critical vulnerability in the Merkle-Patricia Trie (MPT) proof verification library. The bug allowed forging proofs of data absence in storage — an attacker could falsify oracle prices, forge voting power, or directly steal funds.

The vulnerability affected Aave, Frax, StakeDAO and other protocols using cross-chain state verification. The ChainSecurity post-mortem details the mechanics: with a truncated proof path, the function returned an empty array instead of reverting, which was interpreted as valid proof.

Responsible disclosure: March 11–14 — verification and identification of affected contracts, March 14–15 — protocol notifications, March 31 — public disclosure. Losses were avoided.

At ETH Belgrade, Curve presented Block Oracle — a modular framework for secure cross-chain messaging. The system operates on 20+ networks, prioritizing native bridges with LayerZero as fallback. Architecture: blockhash transport → MPT proofs → verification. Code in Vyper, audits by Cyfrin and ChainSecurity.

June 4 — As part of Belgrade Blockchain Week, Curve Ecosystem Day took place. Over 150 participants, up to 50 people per session. Format — open dialogue without marketing, only professional content.

Michael Egorov presented Yield Basis — a protocol for sustainable yield on tokenized BTC and ETH through spot leverage. Speakers from Aragon, Liquity, Status, Tenderly, DeFi Saver. Topics: cross-chain infrastructure, yield-bearing stablecoins, veTokenomics, liquidity UX.

DAO Treasury: Protocol's Own Reserves

June 27 — The DAO voted to create a Treasury — reserves receiving 10% of all protocol fees. Unlike the community fund, these funds have no vesting and can be quickly directed to development, audits, bug bounties, and other DAO priorities.

Q3 — a quarter of maturity and expansion. August 12 — Curve DAO turned five years old; CRV emissions decreased by 15.9% according to the smart contract program. Revenue doubled to $7.3M, trading volume — $29B. Robinhood listed CRV — $300M volume in the first 24 hours. FXSwap opened the path to on-chain forex. Yield Basis launched and changed the rules for Bitcoin liquidity. Cross-chain boost via Block Oracle gave veCRV holders boost on any network. Curve integrated into Telegram via TAC — access to a billion users. Presence expanded to Plasma and Etherlink.

Q3 demonstrated sustainable growth after Q2's challenges. Protocol revenue doubled — from $3.9M to $7.3M, fully distributed to veCRV holders. Trading volume reached $29B. A strong signal before the record-breaking Q4.

DNS attack recovery completed. Ecosystem operating at full capacity.

In July, cross-chain boost launched — the ability to receive enhanced CRV rewards on any network, not just Ethereum.

Technically, this became possible thanks to Curve Block Oracle — public infrastructure for transmitting storage proofs between networks. The system broadcasts veCRV balances to 20+ blockchains, allowing LPs on L2s and sidechains to receive up to 2.5x boost.

First major integrators: StakeDAO (full support via OnlyBoost) and Convex (partial integration). For veCRV holders, this means: lock on Ethereum, boost everywhere.

July 15 — Curve integrated into the Telegram ecosystem via TAC (TON Application Chain) — an EVM-compatible L1 based on CosmosEVM. Over a billion Telegram users gained access to Curve liquidity. A strategic step toward mass adoption.

July 24 — Michael Egorov became the fifth bearer of the Ethereum Torch — a relay recognizing contributions to the Ethereum ecosystem. The creator of Curve joined the list of key figures shaping the decentralized future of the world.

frxUSD Becomes a crvUSD PegKeeper

August 1 — LlamaRisk published a risk review of frxUSD for PegKeeper — recommending adding frxUSD to the crvUSD stabilization system with an initial limit of $3M.

PegKeeper automatically mints/burns crvUSD to maintain the peg. Adding frxUSD expands this mechanism: Frax's yield-forwarding model combined with PegKeeper mechanics creates additional yield for veCRV. By Q4, the new pool grew to $41M TVL.

August 7 — Curve deployed on Etherlink, an EVM-compatible package built on the Tezos protocol.

Also September 25 — Curve launched on Plasma — a next-generation L1 from Tether and Bitfinex, optimized for stablecoin payments. Plasma offers zero-fee transactions and instant settlements. Curve provides critical liquidity for stablecoin pools. Result: $25M TVL in the first week. For Curve, this is a strategic partnership: access to payment and remittance infrastructure backed by institutional players (Peter Thiel, Paolo Ardoino).

August 12 — a historic date. Exactly five years ago, the CRV token was deployed, and the emission program was permanently written into the code.

With the five-year anniversary, CRV emissions decreased by 15.9% — from ~137.4M to ~115.5M tokens per year. Current inflation: 4.92% annually. This wasn't a team decision — it's the execution of an immutable smart contract created on August 12, 2020. Inflation will continue to decrease every August until emissions are exhausted in 200+ years.

Five years in DeFi is an epoch. Curve has weathered it, becoming the infrastructure that others build on — the base liquidity layer for all of DeFi.

Spectra Finance — a yield derivatives protocol — launched a market based on scrvUSD. Mechanics: yield is split into Principal Token (base asset) and Yield Token (right to future yield). Traders can lock in rates or speculate on changes.

Spectra TVL grew from $20M to $100M over the year. Curve receives 20% of all swap fees from Spectra pools.

September 4 — Curve introduced FXSwap — a next-generation AMM for currency pairs and low-volatility assets.

Historically, FX pairs suffered from insufficient DEX liquidity: concentrated liquidity requires constant adjustments and carries risks for LPs. FXSwap solves this problem through the external refuel mechanism — an external capital flow maintaining depth near market price.

The first pool — ZCHF/crvUSD (Swiss franc from Frankencoin against crvUSD) — showed up to 100% APY in CRV incentives. TVL tripled in a week. FXSwap technology became the foundation for Yield Basis.

Strategic significance: Curve moves beyond stablecoins into on-chain forex, opening the path to tokenized RWA — gold, silver, and beyond.

September 18 — Robinhood added CRV to its platform — millions of retail investors in the US gained trading access.

Market reaction was immediate: CRV trading volume exceeded $300M in the first 24 hours, price rose 10%+. Listing on a regulated platform of this scale — recognition of protocol maturity and expansion of the token holder base.

September 24 — Yield Basis launched — a next-generation protocol integrated into Curve, solving the impermanent loss problem through a liquidity leverage mechanism.

The idea is revolutionary: with 2x leverage automatically maintained by the system, impermanent loss virtually disappears. This opens the path to sustainable yield for LPs, primarily for Bitcoin.

Revenue for Curve:

Yield Basis allocates 25% of YB to Curve, which Yield Basis liquidity providers receive.

Curve receives 35% to 65% of the fees that veYB holders earn.

Q4 cemented Curve's leadership. 44% of all DEX fees on Ethereum — 27x growth in one year. 30-day fees reached $15.1M. Record active users — 56.6K. crvUSD tripled to $331M and passed the stress test during $19B in liquidations. Three BTC pools — TOP-3 by TVL among all DEXs ($409M). The DAO voted for a $1B credit line for Yield Basis with record quorum. PegKeeper received triple capacity. Emergency DAO expanded authority. Curve joined EPAA. Monad became the 28th network.

October 15 — Binance and numerous other exchanges listed the YB token (Yield Basis) — and the Bitcoin liquidity flywheel on Curve began spinning. By end of December, three BTC pools occupied top positions among all DEXs:

crvUSD-cbBTC: $205M

crvUSD-WBTC: $103M

crvUSD-tBTC: $101M

Total $409M in BTC liquidity — Michael Egorov's vision of the "Bitcoin black hole" is becoming reality.

Multi-Chain Expansion

November 24 — Curve launched on Monad — a next-generation high-performance L1 with 10,000 TPS. Curve became one of 13 launch applications on mainnet launch day — confirmation of "most desired DEX" status for new blockchains.

By year-end, Curve was present on 28 EVM-compatible networks.

This was made possible by Curve-Lite — an open-source solution for express deployment, developed at the end of 2024.

Q4 brought record fees. In December, 30-day fees reached $15.1M — nearly 10x growth from 2023 lows.

December 19 — The official press release with a key figure: Curve now generates 44% of all DEX fees on Ethereum. A year ago, this figure was 1.6%. 27x growth in 12 months — this isn't a fluctuation, it's a structural market shift.

Growth drivers: crvUSD supply tripled to $331M (from $124M in Q3) thanks to Yield Basis demand.

Curve recorded an all-time high Monthly Active Users — 56.6 thousand. More users — more transactions — more fees for veCRV holders. Adoption growth directly converts to ecosystem revenue.

In December, the DAO voted to expand the crvUSD credit line for Yield Basis from $60M to $1 billion — an unprecedented scale of trust.

The vote set a record quorum in veCRV history. An overwhelming majority supported the proposal. This is a signal: the community believes in the Bitcoin liquidity strategy and is ready to scale it aggressively.

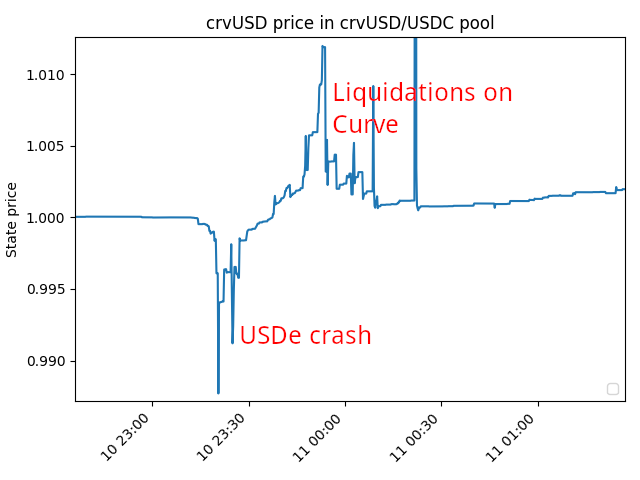

October 10 — a day of massive liquidations in the crypto market: $19B in positions closed in 24 hours. crvUSD passed the stress test: peg held in the 0.996–1.012 range (excluding MEV). Curve liquidity and pool-based oracle system provided stability where other stablecoins faced pressure.

frxUSD/crvUSD PegKeeper reached $41M TVL. LlamaRisk Optimizer Vault on IPOR Fusion. Sky deployed stUSDS/USDS pools with 500K USDS incentives. XDC DeFi Surge doubled network TVL to $24M.

Following the October 14 vote on YB credit line expansion, the DAO increased PegKeeper limits by 3x:

crvUSD/USDC: 45M → 135M

crvUSD/USDT: 45M → 135M

crvUSD/pyUSD: 15M → 45M

crvUSD/frxUSD: 3M → 9M

Capacity expansion — a response to growing crvUSD supply and preparation for scaling through Yield Basis.

November 5 — Curve joined the Ethereum Protocol Advocacy Alliance (EPAA) — a coalition of DeFi protocols representing ecosystem interests in Ethereum's development. Strategic participation in shaping the future of the base layer.

November 12 — Proposal 1252 passed — Emergency DAO received expanded control over critical parameters: debt ceilings, AMM fees, monetary policy, deposit limits for Mint Factory, Controller, and Vaults. This allows faster response to market conditions without a full governance cycle.

December 24 — The DAO rejected the initial proposal for 17.45M CRV for Swiss Stake AG (54.46% against). Off-chain collaboration led to a compromise:

December 29 — the modified proposal with phased vesting was approved.

An example of mature governance: the ability to say "no," discuss terms, and find a solution that satisfies all parties.

In 2025, YB processed $1.63B in volume, demonstrating its success and viability.

At the end of December, the Yield Basis 2026 Thesis was released: analytical work examining protocol expansion into ETH markets. As well as markets for gold, silver, tokenized stocks — assets that until now lacked meaningful on-chain liquidity due to impermanent loss.

Proposal 1299 optimizes FX and YB pools, reducing value loss to arbitrage traders during rebalancing. This update needs approval before adding ETH and other assets to Yield Basis.

2025 in numbers: DEX fee share on Ethereum grew to 44%, crvUSD tripled to $331M, active loans exceeded $300M, presence expanded to 28 networks, monthly active users reached a record 56.6K.

Key events: Yield Basis and FXSwap launch, cross-chain boost for veCRV, veCRV whitelist removal, launch on 9 new blockchains. crvUSD passed the stress test. The protocol survived a DNS attack, processing $400M+ volume while the frontend was unavailable. The DAO created a treasury and expanded Emergency DAO. Curve joined EPAA. In August, celebrated its fifth anniversary.

Technologies of the year: Yield Basis solved impermanent loss for volatile assets. FXSwap opened on-chain forex. Cross-chain boost via Block Oracle gave veCRV holders boost across all networks. Curve-Lite enabled rapid deployment on new networks. Curve's ve-model became the industry standard through Aragon toolkit.

2026: LlamaLend V2 with LP/PT collateral support. Yield Basis expansion to gold, silver, stocks, and ETH. FXSwap as the primary on-chain forex venue. Block Oracle development as public infrastructure. UI modernization and continued multi-chain expansion.

Happy New Year 2026! Thank you to the community for your support — together we are building the future of DeFi.

As we reflect on 2025, let's highlight the key milestones and inspiring achievements.

A year ago, Curve generated 1.6% of DEX fees on Ethereum. Today it's 44%. A 27x increase in 12 months.

In 2024, we launched LlamaLend and scrvUSD. In 2025, these products transformed the market and became the foundation for new breakthroughs. The launch of Yield Basis turned Curve into the largest Bitcoin liquidity hub. crvUSD supply tripled to $331M. FXSwap opened the door to on-chain forex.

While dominating Ethereum, the protocol continued its multi-chain expansion — nine new networks in one year, thanks to the simplicity and convenience of Curve-Lite.

These and many other important events are covered in this report — quarter by quarter.

Q1

Q2

Q3

Q4

Q1 set the pace for the entire year. $35 billion in trading volume — the best quarter in protocol history at that time. Transactions tripled: from 1.8M to 5.5M. A record achieved against a 20% market downturn. LlamaLend doubled its TVL to $84M thanks to the Resupply launch. crvUSD gained $80M in new capacity through Bitcoin collaterals. JPMorgan forecasted yield-bearing stablecoins to grow from 6% to 50% of the market — with scrvUSD in focus. Aragon integrated the ve-model into their toolkit. The industry acknowledged: Curve technology is the standard.

January 7 — Curve deployed on Sonic — a high-performance L1 with 10,000+ TPS. Curve provided critical DEX infrastructure from day one of the network's operation.

February 17 — LlamaRisk launched Market Health Scores — seven market health metrics for crvUSD. Clear risks for LPs, predictability for borrowers, objective foundation for the DAO.

March 12 — crvUSD received three new collaterals and $80M in capacity: cbBTC (50M), weETH (20M), LBTC (10M). Two Bitcoin collaterals strengthened crvUSD's position as the stablecoin for BTC holders.

March 20 — Resupply Protocol launched — a subDAO from Convex and Yearn. The mechanics are elegant: crvUSD deposits in LlamaLend continue to earn yield and CRV incentives (with boost via Convex), while simultaneously serving as collateral for minting reUSD.

First week: $44.7K in fees, $35M reUSD minted against $42M collateral. By April, total fees reached $345K. The flywheel spun up — demand for scrvUSD pushed LlamaLend TVL from $38M to $84M in a matter of days.

March 27 — JPMorgan analysts forecasted yield-bearing stablecoins to grow from 6% to 50% of the market. The driver — the ability to earn yield without trading or lending risks. scrvUSD — the yield-bearing wrapper of crvUSD — is positioned at the center of this trend.

March 27 — Aragon integrated Curve's ve-model into their Value Accrual Toolkit. Vote Escrow (locking tokens for votes) and Gauges (distributing incentives through voting) — key components borrowed from Curve. The toolkit is already used by Mode, Puffer, Bedrock. Curve technologies have become the industry standard.

Q2 put Curve to the test. Two security incidents — an X account hack and a DNS attack — didn't stop the protocol: $400M in volume was processed while the frontend was unavailable. Meanwhile, LlamaLend showed explosive growth: TVL +228%, borrowed volume +104.5%. Three new networks, veCRV whitelist removal, record crvUSD supply. A quarter that hardened the ecosystem.

Strategic USD Reserves: New Foundation

In April, the DAO voted to adopt the USDC/USDT pool as the official Basepool — the foundation for creating new stablecoin pools called Strategic Reserves.

This was a strategic move. The old 3pool (DAI/USDC/USDT) served as the ecosystem's foundation for years, but MakerDAO migrated from DAI to USDS. Time for an upgrade.

The new Basepool uses StableSwap-NG with an amplification coefficient of 20,000 (versus ~2,000 for 3pool) — an order of magnitude more concentrated liquidity. Fees reduced to 0.003%.

Result: the pool processes ~$27M in daily volume with only $6.3M TVL — capital efficiency of 4-5x.

crvUSD: Record Supply

May 8 — crvUSD reached $179.8M in circulation — a record at the time (soon to double again). A week later, the stablecoin celebrated its 2nd anniversary.

For Curve, this isn't just a number: every minted crvUSD generates borrowing fees that go to veCRV holders. More supply — more revenue for the ecosystem.

May 26 — The DAO voted to remove the veCRV whitelist — now any smart contract can lock CRV. Previously, only Convex, Yearn, and StakeDAO participated in the ve-mechanism.

Democratization strengthens the flywheel: more protocols locking CRV → stronger demand → higher value for all holders.

Q2 brought new launches on three networks: May 27 — Plume Network (RWAfi L1), June 6 — Hyperliquid (perpetual trading L1), June 12 — XDC Network (enterprise trade finance).

Q2 was a turning point for Curve lending. According to the LlamaRisk report, borrowed crvUSD volume grew by 104.5% (from $33.5M to $68.7M). Average LlamaLend TVL increased by 228% — from $46M in Q1 to $151M in Q2.

By the end of June, borrowed volume reached $126M with 766 active positions. LlamaLend became one of the most efficient and affordable lending platforms in DeFi — large borrowers migrated for competitive rates, liquidation protection, and high capital efficiency.

Technical improvements: EMAMonetaryPolicy for markets with yield-bearing assets, ProxyOracle for flexible deployment of new markets. crvUSD peg stability improved by 66% — daily deviation reduced to 3.9 BPS. By year-end, active loans exceeded $300M.

Q2 will be remembered not only for innovations. Two security incidents — and neither stopped the protocol.

X Account Hack

May 5 — Attackers gained access to the official @CurveFinance account on X and posted a phishing link to the "first CRV airdrop." Founder Michael Egorov responded immediately: "Confirmed: Curve X account hacked." Control was restored the same day.

DNS Attack: A Turning Point

May 12 — Attackers gained access to the DNS registrar and redirected curve.fi traffic to a phishing site.

But here's the remarkable part: while the frontend was unavailable, the protocol processed over $400M in volume. Contracts continued working. The team migrated to a new domain curve.finance. The incident became an impetus for infrastructure strengthening.

March 11 — Roman Agureev, a Curve researcher, discovered a critical vulnerability in the Merkle-Patricia Trie (MPT) proof verification library. The bug allowed forging proofs of data absence in storage — an attacker could falsify oracle prices, forge voting power, or directly steal funds.

The vulnerability affected Aave, Frax, StakeDAO and other protocols using cross-chain state verification. The ChainSecurity post-mortem details the mechanics: with a truncated proof path, the function returned an empty array instead of reverting, which was interpreted as valid proof.

Responsible disclosure: March 11–14 — verification and identification of affected contracts, March 14–15 — protocol notifications, March 31 — public disclosure. Losses were avoided.

At ETH Belgrade, Curve presented Block Oracle — a modular framework for secure cross-chain messaging. The system operates on 20+ networks, prioritizing native bridges with LayerZero as fallback. Architecture: blockhash transport → MPT proofs → verification. Code in Vyper, audits by Cyfrin and ChainSecurity.

June 4 — As part of Belgrade Blockchain Week, Curve Ecosystem Day took place. Over 150 participants, up to 50 people per session. Format — open dialogue without marketing, only professional content.

Michael Egorov presented Yield Basis — a protocol for sustainable yield on tokenized BTC and ETH through spot leverage. Speakers from Aragon, Liquity, Status, Tenderly, DeFi Saver. Topics: cross-chain infrastructure, yield-bearing stablecoins, veTokenomics, liquidity UX.

DAO Treasury: Protocol's Own Reserves

June 27 — The DAO voted to create a Treasury — reserves receiving 10% of all protocol fees. Unlike the community fund, these funds have no vesting and can be quickly directed to development, audits, bug bounties, and other DAO priorities.

Q3 — a quarter of maturity and expansion. August 12 — Curve DAO turned five years old; CRV emissions decreased by 15.9% according to the smart contract program. Revenue doubled to $7.3M, trading volume — $29B. Robinhood listed CRV — $300M volume in the first 24 hours. FXSwap opened the path to on-chain forex. Yield Basis launched and changed the rules for Bitcoin liquidity. Cross-chain boost via Block Oracle gave veCRV holders boost on any network. Curve integrated into Telegram via TAC — access to a billion users. Presence expanded to Plasma and Etherlink.

Q3 demonstrated sustainable growth after Q2's challenges. Protocol revenue doubled — from $3.9M to $7.3M, fully distributed to veCRV holders. Trading volume reached $29B. A strong signal before the record-breaking Q4.

DNS attack recovery completed. Ecosystem operating at full capacity.

In July, cross-chain boost launched — the ability to receive enhanced CRV rewards on any network, not just Ethereum.

Technically, this became possible thanks to Curve Block Oracle — public infrastructure for transmitting storage proofs between networks. The system broadcasts veCRV balances to 20+ blockchains, allowing LPs on L2s and sidechains to receive up to 2.5x boost.

First major integrators: StakeDAO (full support via OnlyBoost) and Convex (partial integration). For veCRV holders, this means: lock on Ethereum, boost everywhere.

July 15 — Curve integrated into the Telegram ecosystem via TAC (TON Application Chain) — an EVM-compatible L1 based on CosmosEVM. Over a billion Telegram users gained access to Curve liquidity. A strategic step toward mass adoption.

July 24 — Michael Egorov became the fifth bearer of the Ethereum Torch — a relay recognizing contributions to the Ethereum ecosystem. The creator of Curve joined the list of key figures shaping the decentralized future of the world.

frxUSD Becomes a crvUSD PegKeeper

August 1 — LlamaRisk published a risk review of frxUSD for PegKeeper — recommending adding frxUSD to the crvUSD stabilization system with an initial limit of $3M.

PegKeeper automatically mints/burns crvUSD to maintain the peg. Adding frxUSD expands this mechanism: Frax's yield-forwarding model combined with PegKeeper mechanics creates additional yield for veCRV. By Q4, the new pool grew to $41M TVL.

August 7 — Curve deployed on Etherlink, an EVM-compatible package built on the Tezos protocol.

Also September 25 — Curve launched on Plasma — a next-generation L1 from Tether and Bitfinex, optimized for stablecoin payments. Plasma offers zero-fee transactions and instant settlements. Curve provides critical liquidity for stablecoin pools. Result: $25M TVL in the first week. For Curve, this is a strategic partnership: access to payment and remittance infrastructure backed by institutional players (Peter Thiel, Paolo Ardoino).

August 12 — a historic date. Exactly five years ago, the CRV token was deployed, and the emission program was permanently written into the code.

With the five-year anniversary, CRV emissions decreased by 15.9% — from ~137.4M to ~115.5M tokens per year. Current inflation: 4.92% annually. This wasn't a team decision — it's the execution of an immutable smart contract created on August 12, 2020. Inflation will continue to decrease every August until emissions are exhausted in 200+ years.

Five years in DeFi is an epoch. Curve has weathered it, becoming the infrastructure that others build on — the base liquidity layer for all of DeFi.

Spectra Finance — a yield derivatives protocol — launched a market based on scrvUSD. Mechanics: yield is split into Principal Token (base asset) and Yield Token (right to future yield). Traders can lock in rates or speculate on changes.

Spectra TVL grew from $20M to $100M over the year. Curve receives 20% of all swap fees from Spectra pools.

September 4 — Curve introduced FXSwap — a next-generation AMM for currency pairs and low-volatility assets.

Historically, FX pairs suffered from insufficient DEX liquidity: concentrated liquidity requires constant adjustments and carries risks for LPs. FXSwap solves this problem through the external refuel mechanism — an external capital flow maintaining depth near market price.

The first pool — ZCHF/crvUSD (Swiss franc from Frankencoin against crvUSD) — showed up to 100% APY in CRV incentives. TVL tripled in a week. FXSwap technology became the foundation for Yield Basis.

Strategic significance: Curve moves beyond stablecoins into on-chain forex, opening the path to tokenized RWA — gold, silver, and beyond.

September 18 — Robinhood added CRV to its platform — millions of retail investors in the US gained trading access.

Market reaction was immediate: CRV trading volume exceeded $300M in the first 24 hours, price rose 10%+. Listing on a regulated platform of this scale — recognition of protocol maturity and expansion of the token holder base.

September 24 — Yield Basis launched — a next-generation protocol integrated into Curve, solving the impermanent loss problem through a liquidity leverage mechanism.

The idea is revolutionary: with 2x leverage automatically maintained by the system, impermanent loss virtually disappears. This opens the path to sustainable yield for LPs, primarily for Bitcoin.

Revenue for Curve:

Yield Basis allocates 25% of YB to Curve, which Yield Basis liquidity providers receive.

Curve receives 35% to 65% of the fees that veYB holders earn.

Q4 cemented Curve's leadership. 44% of all DEX fees on Ethereum — 27x growth in one year. 30-day fees reached $15.1M. Record active users — 56.6K. crvUSD tripled to $331M and passed the stress test during $19B in liquidations. Three BTC pools — TOP-3 by TVL among all DEXs ($409M). The DAO voted for a $1B credit line for Yield Basis with record quorum. PegKeeper received triple capacity. Emergency DAO expanded authority. Curve joined EPAA. Monad became the 28th network.

October 15 — Binance and numerous other exchanges listed the YB token (Yield Basis) — and the Bitcoin liquidity flywheel on Curve began spinning. By end of December, three BTC pools occupied top positions among all DEXs:

crvUSD-cbBTC: $205M

crvUSD-WBTC: $103M

crvUSD-tBTC: $101M

Total $409M in BTC liquidity — Michael Egorov's vision of the "Bitcoin black hole" is becoming reality.

Multi-Chain Expansion

November 24 — Curve launched on Monad — a next-generation high-performance L1 with 10,000 TPS. Curve became one of 13 launch applications on mainnet launch day — confirmation of "most desired DEX" status for new blockchains.

By year-end, Curve was present on 28 EVM-compatible networks.

This was made possible by Curve-Lite — an open-source solution for express deployment, developed at the end of 2024.

Q4 brought record fees. In December, 30-day fees reached $15.1M — nearly 10x growth from 2023 lows.

December 19 — The official press release with a key figure: Curve now generates 44% of all DEX fees on Ethereum. A year ago, this figure was 1.6%. 27x growth in 12 months — this isn't a fluctuation, it's a structural market shift.

Growth drivers: crvUSD supply tripled to $331M (from $124M in Q3) thanks to Yield Basis demand.

Curve recorded an all-time high Monthly Active Users — 56.6 thousand. More users — more transactions — more fees for veCRV holders. Adoption growth directly converts to ecosystem revenue.

In December, the DAO voted to expand the crvUSD credit line for Yield Basis from $60M to $1 billion — an unprecedented scale of trust.

The vote set a record quorum in veCRV history. An overwhelming majority supported the proposal. This is a signal: the community believes in the Bitcoin liquidity strategy and is ready to scale it aggressively.

October 10 — a day of massive liquidations in the crypto market: $19B in positions closed in 24 hours. crvUSD passed the stress test: peg held in the 0.996–1.012 range (excluding MEV). Curve liquidity and pool-based oracle system provided stability where other stablecoins faced pressure.

frxUSD/crvUSD PegKeeper reached $41M TVL. LlamaRisk Optimizer Vault on IPOR Fusion. Sky deployed stUSDS/USDS pools with 500K USDS incentives. XDC DeFi Surge doubled network TVL to $24M.

Following the October 14 vote on YB credit line expansion, the DAO increased PegKeeper limits by 3x:

crvUSD/USDC: 45M → 135M

crvUSD/USDT: 45M → 135M

crvUSD/pyUSD: 15M → 45M

crvUSD/frxUSD: 3M → 9M

Capacity expansion — a response to growing crvUSD supply and preparation for scaling through Yield Basis.

November 5 — Curve joined the Ethereum Protocol Advocacy Alliance (EPAA) — a coalition of DeFi protocols representing ecosystem interests in Ethereum's development. Strategic participation in shaping the future of the base layer.

November 12 — Proposal 1252 passed — Emergency DAO received expanded control over critical parameters: debt ceilings, AMM fees, monetary policy, deposit limits for Mint Factory, Controller, and Vaults. This allows faster response to market conditions without a full governance cycle.

December 24 — The DAO rejected the initial proposal for 17.45M CRV for Swiss Stake AG (54.46% against). Off-chain collaboration led to a compromise:

December 29 — the modified proposal with phased vesting was approved.

An example of mature governance: the ability to say "no," discuss terms, and find a solution that satisfies all parties.

In 2025, YB processed $1.63B in volume, demonstrating its success and viability.

At the end of December, the Yield Basis 2026 Thesis was released: analytical work examining protocol expansion into ETH markets. As well as markets for gold, silver, tokenized stocks — assets that until now lacked meaningful on-chain liquidity due to impermanent loss.

Proposal 1299 optimizes FX and YB pools, reducing value loss to arbitrage traders during rebalancing. This update needs approval before adding ETH and other assets to Yield Basis.

2025 in numbers: DEX fee share on Ethereum grew to 44%, crvUSD tripled to $331M, active loans exceeded $300M, presence expanded to 28 networks, monthly active users reached a record 56.6K.

Key events: Yield Basis and FXSwap launch, cross-chain boost for veCRV, veCRV whitelist removal, launch on 9 new blockchains. crvUSD passed the stress test. The protocol survived a DNS attack, processing $400M+ volume while the frontend was unavailable. The DAO created a treasury and expanded Emergency DAO. Curve joined EPAA. In August, celebrated its fifth anniversary.

Technologies of the year: Yield Basis solved impermanent loss for volatile assets. FXSwap opened on-chain forex. Cross-chain boost via Block Oracle gave veCRV holders boost across all networks. Curve-Lite enabled rapid deployment on new networks. Curve's ve-model became the industry standard through Aragon toolkit.

2026: LlamaLend V2 with LP/PT collateral support. Yield Basis expansion to gold, silver, stocks, and ETH. FXSwap as the primary on-chain forex venue. Block Oracle development as public infrastructure. UI modernization and continued multi-chain expansion.

Curve Finance Unofficial

Curve Finance Unofficial

No comments yet