Tokenization is already changing how markets behave onchain. It turns RWAs into programmable assets that can move 24/7, settle fast, and be reused across lending, borrowing, leverage, hedging, and liquidity management.

It also changes how these assets are distributed, accessed, and tracked. In DeFi, the key step beyond “holding” is reuse - the same asset can be used across multiple protocols. Collateral is the clearest example: you can keep exposure to an underlying asset while borrowing liquidity against it.

Private credit is a strong starting point because it’s typically structured as ‘buy-and-hold’, with limited secondary liquidity. When positions change hands, it’s often a one-to-one transfer between a seller and a specific buyer. If a private credit position can be used as collateral, it becomes usable inside onchain lending markets - not just a standalone yield position.

That is what ‘composable private credit’ is about.

Composable private credit means a private credit position can be composed into other DeFi actions - e.g. posted as collateral in lending markets - so an investor can access liquidity without selling the underlying credit exposure.

The closest TradFi analogy is repo: post collateral, borrow short-term liquidity, keep exposure.

Why it matters:

Liquidity without selling: borrow stablecoins while staying invested in the credit position

Reuse: the same credit position can support additional strategies (within risk limits)

Integration: once an asset is usable across DeFi, it becomes easier to plug into wallets, vaults, and structured products

Morpho has been documenting this “RWA playbook” with multiple live markets, including private credit and credit funds.

Using a private credit position as DeFi collateral works best if three layers line up, and each layer is owned by a different party.

The real-world loan - who owes what, on what terms, how it’s monitored, and what happens in the event of default.

Who underwrites the borrower and sets terms

How reporting is produced and shared

What happens in a default event (cure periods, enforcement, workout)

Why the legal structure is enforceable

If this layer is weak, the onchain wrapper does not save it.

The onchain ‘receipt token’ - what it represents, who can hold or move it, and how mint/redeem works.

Is the receipt token transferable?

Who can mint/redeem, and under what rules?

What permissioning exists (if any), for example KYC at the primary market level

This layer turns “a credit position” into “an asset you can post as collateral”

The borrowing rulebook - how the token is priced, how much can be borrowed against it, and what happens if limits are breached.

This is where “credit becomes collateral” in practice:

How the token is priced

How much can be borrowed against it (LLTV / LTV limits)

Liquidation mechanics and incentives

Caps and guardrails

Monitoring and parameter discipline, often handled by specialist risk teams, like Gauntlet

A simple way to think about it: Layer A defines what the credit claim is and how it’s enforced. Layer B turns that claim into a 'receipt token' that can be held and transferred onchain. Layer C sets the borrowing rules against that token (pricing, LTV limits, and liquidations).

Markets on Morpho are permissionless, immutable and are defined by five fixed parameters set at creation:

Loan asset

Collateral asset

Oracle

Interest rate model

LLTV (Liquidation Loan-to-Value)

When creating a new market on Morpho, these parameters allow credit tokens (‘receipt tokens’) to function as DeFi collateral.

Every Morpho Market has two sides:

Supply side: Morpho Vault suppliers provide liquidity which in turn gets allocated to markets based on the vault allocation set by the curator, earning yield based on lending activity.

E.g., for the AA_FalconXUSDC/USDC Market on Morpho, Gauntlet USDC Frontier and Gauntlet USDC RWA allocate USDC liquidity and direct it to this market.Borrow side: borrowers on Morpho supply collateral to borrow against the available liquidity, paying interest that is distributed as yield back to vault suppliers.

E.g. the Aera Vault on Gauntlet makes up most of the AA_FalconXUSDC/USDC Market, depositing AA_FalconXUSDC as collateral to borrow USDC - and in turn using that USDC to increase its exposure to the FalconX Credit Vault on Pareto and compound returns.

While the market itself is immutable, Gauntlet’s optimization engine can actively adjust leverage at the Aera Vault level in response to market conditions. Parameters such as target LTV, LTV wiggle room, and minimum yield spread give Gauntlet's engine the levers to tighten or extend the loop - scaling up when conditions are favorable and automatically unwinding when the spread compresses.

This case study covers a working example of tokenized private credit being used as collateral in a DeFi lending market.

Structure and roles:

FalconX is the main credit counterparty behind the FalconX Credit Vault on Pareto

M11Credit curates the Credit Vault (credit oversight and reporting)

Pareto provides the credit infrastructure behind the Credit Vault, including the onchain vault mechanics and issuance of the receipt token, AA_FalconXUSDC

Keyring provides zero-knowledge KYC verification for new depositors on Pareto

Morpho is where AA_FalconXUSDC is supplied as collateral to borrow USDC

Gauntlet created the AA_FalconXUSDC/USDC Market on Morpho, and launched a levered FalconX strategy on its Aera Vault infrastructure that allows AA_FalxonXUSDC suppliers to get amplified exposure within strict risk parameters

How the flow works:

USDC is deposited into the FalconX Credit Vault on Pareto, which mints the receipt token AA_FalconXUSDC to the depositor

AA_FalconXUSDC is supplied into the automated Aera Vault on Gauntlet. The vault uses AA_FalconXUSDC tokens as collateral on Morpho, and borrows USDC against it

The borrowed USDC is automatically deposited into the FalconX Credit Vault on Pareto, creating a looped position that amplifies yield exposure

Gauntlet’s quantitative engine dynamically manages leverage, adjusting exposure based on real-time yield, borrow rates, and market risk

The Gauntlet Levered FalconX Strategy has yielded over 13% in APY since inception, and built up this market fully as it currently borrows $30.8m in USDC for $59.3m in levered collateral, for a net TVL of $28.5m.

$51M in levered collateral. $26M in borrows. $25M in net TVL.

$40M in liquidity supply from Gauntlet-curated vaults.

Built on Aera and launched in August 2025,

The strategy uses Pareto FalconX Credit Vault (CV) tokens as collateral to borrow USDC and buy more CV tokens within strict risk

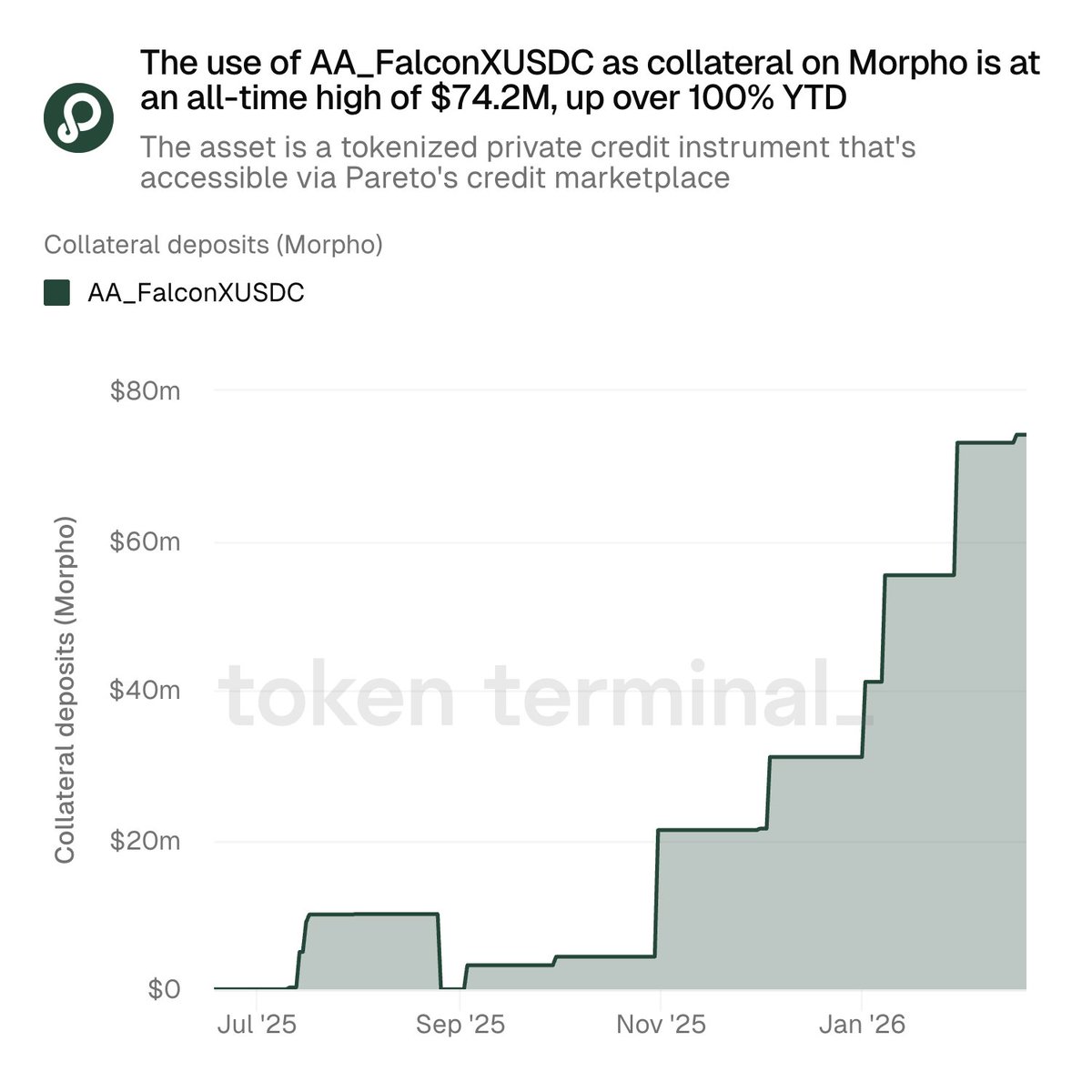

AA_FalconXUSDC collateral on Morpho has reached over $74m and is up more than 100% year-to-date.

The use of AA_FalconXUSDC as collateral on @Morpho is at an all-time high of $74.2M, up over 100% YTD.

The use of AA_FalconXUSDC as collateral on @Morpho is at an all-time high of $74.2M, up over 100% YTD.The asset is a tokenized private credit instrument that's accessible via @paretocredit's marketplace.

A chart & development to follow

Using private credit as collateral is still early. The next step is making it repeatable across more credit assets, without relying on one-off integrations.

Three areas matter most:

Markets need consistent answers to basic questions: what is being financed, what is the current exposure, which events impact risk and require an update, how often these updates come, and what happens in the event of default. Without this, pricing and risk limits become guesswork.

Credit assets do not trade like liquid tokens. Pricing methods and oracles need to handle slow-moving valuations, stale updates, and event-driven changes. If pricing is weak, leverage limits and liquidations won’t behave predictably.

For collateral to work, there has to be a realistic way to reduce risk when positions move against limits. That can be secondary liquidity, structured redemption mechanics, or liquidation design that has a viable exit - especially during stressed conditions.

As these pieces improve, more structures become possible:

Longer-dated borrowing against credit collateral (not only short-term)

Rate products built on top (fixed/floating, term structure)

Basket collateral (diversified credit exposure instead of single-name)

Managed leverage with strict limits and transparent rules (e.g. Gauntlet-style automations)

The winners will be the credit systems that can prove their assets are good collateral, not just good yield.

Composable private credit changes the role of private credit onchain. It moves from being a passive “hold for yield” position to being an asset that can support real DeFi workflows like borrowing, liquidity management, and risk-controlled leverage.

The automated looping Aera Vault on Gauntlet and AA_FalconXUSDC/USDC Market on Morpho show what this can look like in production. When a credit position has a credible offchain structure, an onchain token representation, and a lending market with disciplined risk parameters, it becomes usable collateral rather than just a wrapped exposure.

The long-term direction is straightforward. If tokenized private credit is going to scale, it will scale through usability as collateral.

We'd like to thank the Gauntlet team for collaborating on this article.

Not financial advice. Always do your own research.

Pareto is an onchain credit infrastructure provider connecting institutional lenders and borrowers. Its whitelabel stack lets partners launch branded credit products without building the lending core from scratch.

Tailored for asset managers, fintechs, and neobanks, Pareto makes credit products programmable by default. It automates loan’s full lifecycle - from onboarding and facility controls to drawdowns/repayments, interest and fee accrual, and reporting - reducing operational overhead while improving transparency and capital efficiency.

As the financial landscape evolves, Pareto aims to set a new standard for institutional credit with fully automated, data-driven lending solutions.

Website | App | X | LinkedIn | Discord | Telegram | Blog

Gauntlet designs modern yield strategies for institutional capital. Fintechs, exchanges, wallets, issuers, and financial institutions use Gauntlet Vaults to drive smarter yields and optimize growth.

Gauntlet Vaults drive risk-adjusted DeFi yields for institutional capital at scale. Strategies are optimized by automated risk platform, designed by the most vigilant, quantitative minds in crypto.